The Mortgage Lead Leak Audit: How AI Sales Agents Find the Revenue Your Funnel is Losing

Most mortgage brokers don't have a lead problem. They have a funnel that leaks.

Discover how a Lead Leak Audit can optimize your mortgage sales funnel and prevent revenue loss with the help of AI Sales Agents.

On this page 7

- The Real Reason Mortgage Brokers Lose Leads

- How to Run a Mortgage Lead Leak Audit

- What an AI Sales Agent Actually Does in a Mortgage Funnel

- The Digital Channel Shift Mortgage Teams Can’t Ignore

- What the Numbers Look Like in Practice

- Running the Audit: Solo Broker vs. Enterprise Operation

- Stop Losing Revenue You Already Paid For

Disclosure: Performance claims and case study results referenced in this article reflect specific client deployments. Individual results vary based on lead volume, market conditions, team configuration, and implementation. Past results do not guarantee future outcomes. This content is intended for licensed mortgage professionals and does not constitute financial or legal advice.

Most mortgage brokers don’t have a lead problem. They have a funnel that leaks.

Here’s what that looks like in practice. You’re running Google Ads, paying for Zillow leads, nurturing referral relationships, and your team is genuinely busy. But your loan volume isn’t growing the way your ad spend would suggest it should. The leads are coming in. They’re just disappearing somewhere between the first inquiry and the submitted application.

McKinsey’s research on the US purchase mortgage market makes the structural diagnosis explicit: banks trail nonbanks in converting customer interest into completed applications, and among the heaviest contributors to that gap are slow response times and cumbersome document requests — the exact friction points that push qualified borrowers toward whoever picks up first. The same research found that only 60% of customers who consider a bank mortgage follow through with the application, compared with 75% for nonbanks.

This is the gap that a Lead Leak Audit is designed to close. Not by generating more traffic, not by hiring more SDRs, but by systematically identifying every stage where a qualified prospect stops engaging — and then building the automated infrastructure to hold them in the funnel until they’re ready to close.

In 2026, the brokers and enterprise lending teams doing this most effectively aren’t relying on follow-up discipline from their human team alone. They’re deploying AI Sales Agents that work leads at every stage, around the clock — with licensed loan officers remaining central to all regulated decisions and borrower consultations.

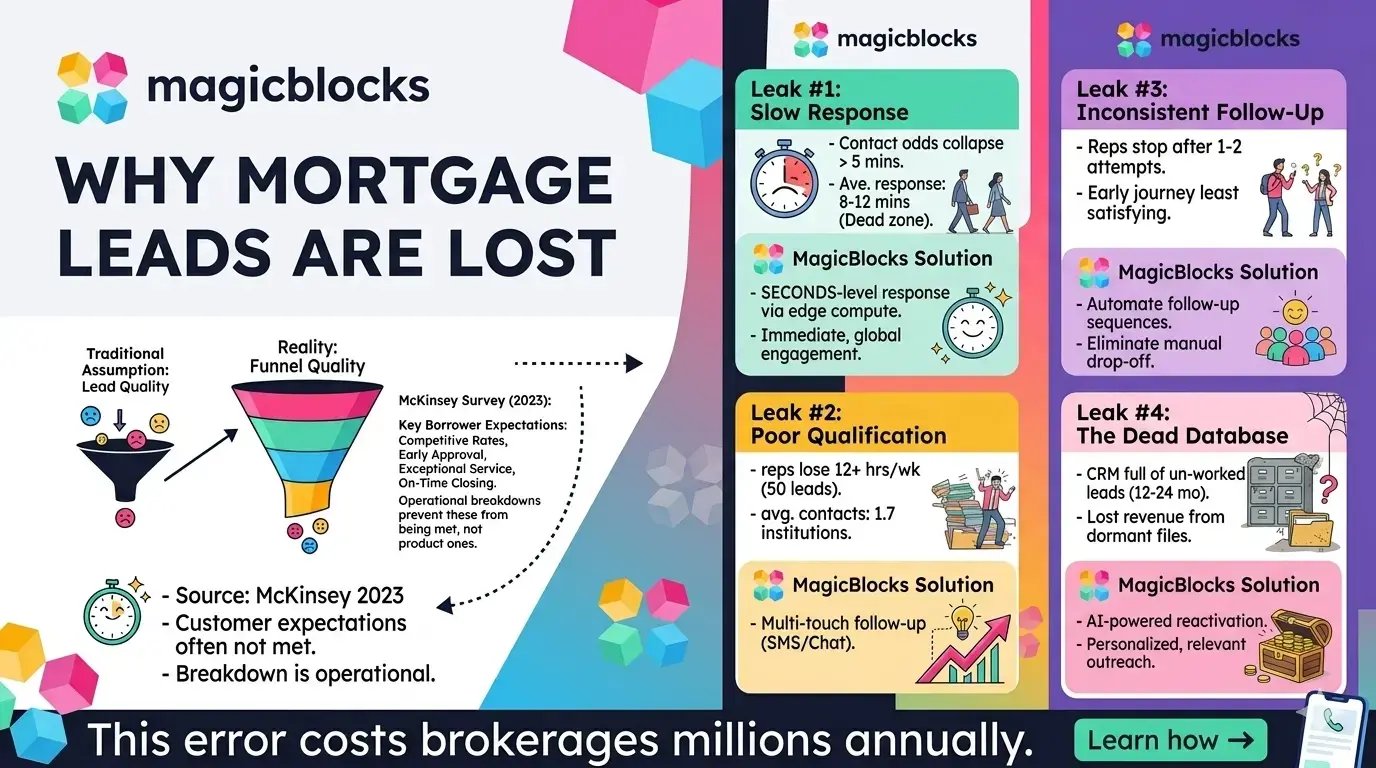

The Real Reason Mortgage Brokers Lose Leads

There’s a default assumption in most lending shops: if a lead doesn’t convert, it wasn’t a good lead. That assumption costs brokerages hundreds of thousands of dollars a year.

The reality is that the quality of the lead matters far less than the quality of the funnel it enters. McKinsey’s 2023 survey of more than 1,100 US purchase-mortgage borrowers found that borrowers’ top expectations of lenders are competitive interest rates, early certainty of approval, exceptional service, and assurance of on-time closing. Most are not being met — and the breakdown is overwhelmingly an operational one, not a product one.

Here are the four places revenue actually escapes in a mortgage sales operation:

Leak #1: Slow Response

Companies that wait longer than five minutes to respond to a new online lead see their odds of contact and qualification collapse compared with those that respond immediately, as shown in research featured in Harvard Business Review’s “The Short Life of Online Sales Leads.”

At 30 minutes, you’re essentially cold-calling someone who raised their hand to speak with you. The average mortgage broker team responds to a new web inquiry in 8 to 12 minutes — which means they’re already operating in the dead zone for most of those leads by the time the first message goes out.

McKinsey’s research on purchase-mortgage borrowers calls out slow response time as one of the heaviest drivers of poor satisfaction scores — and satisfaction scores directly predict whether a borrower completes their application or walks. Satisfied customers are approximately 35% more likely to refinance their mortgage with the same bank than dissatisfied ones.

MagicBlocks AI Sales Agents are built to respond within seconds — via edge compute deployed across 3,000+ global servers — providing immediate first engagement even outside business hours.

Leak #2: Poor Qualification

Your team is spending 15 minutes per lead before they know whether that person is a remotely viable borrower. For a branch with 50 new leads a week, that’s over 12 hours of qualifying work that could be supported by automation. Much of that time is spent on prospects who won’t qualify, aren’t ready, or are just in the early research phase.

McKinsey’s research adds useful context here: just over half of today’s borrowers consider only a single institution in their mortgage search, with the average borrower contacting just 1.7 institutions for information. That means the lender who engages first and qualifies fastest wins the consideration window — often permanently.

An AI Sales Agent can support prequalification through natural conversation — asking about purchase vs. refi intent, rough credit range, target timeline, loan amount, and current lender status — without sounding like a form. The agent captures structured data your loan officers can act on. All final qualification determinations and lending decisions remain with your licensed team.

Leak #3: Inconsistent Follow-Up

Research consistently shows that most sales require multiple follow-up contacts, yet most reps abandon the effort after one or two attempts. That gap is where mortgage brokers lose a significant portion of their ad spend. Leads who don’t answer the first call aren’t necessarily uninterested — they’re busy, they’re comparing options, or the timing was off.

McKinsey’s survey data is particularly sharp here: borrowers evaluating lenders say they are least satisfied with the exploration journey — specifically, the research and inquiry phase before completing the application. This is exactly the window where follow-up depth determines whether a lead converts or disappears.

A human team following up consistently at high volume is difficult to sustain. An AI Sales Agent is built to execute multi-touch follow-up sequences across chat and SMS — reducing the drop-off that occurs when manual outreach lapses.

Leak #4: The Dead Database

Most mortgage CRMs are sitting on 12 to 24 months of leads that were never properly worked. Some were contacted once. Some got stuck in a queue when a loan officer left the company. Some came in at a rate environment that wasn’t favorable and were never re-engaged when conditions changed.

This is potentially recoverable revenue. A meaningful share of dormant leads can re-engage with the right outreach — timing, personalization, and message relevance are the primary drivers. Learn how AI-powered database reactivation works in practice.

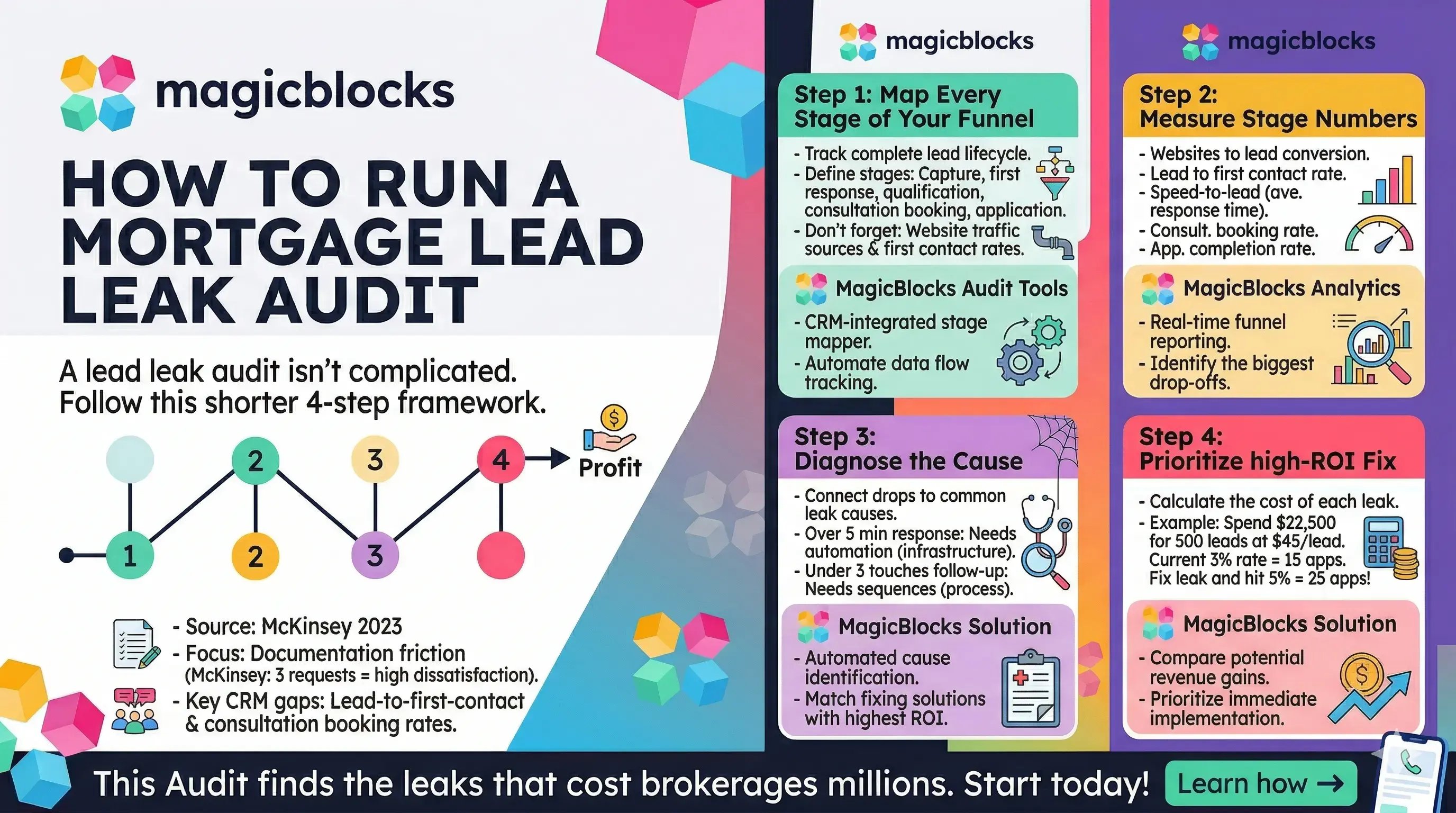

How to Run a Mortgage Lead Leak Audit

A Lead Leak Audit isn’t complicated. It’s a structured review of your funnel’s conversion rates at each stage, followed by a clear identification of which leak is costing you the most. Here’s the framework.

Step 1: Map Every Stage of Your Funnel

Before you can find the leaks, you need a complete picture of the pipe. Document each stage from the moment a lead first appears to the moment a loan closes:

- Traffic source (Google Ads, Zillow, referral, organic)

- Lead capture (web form, phone call, live chat, landing page)

- First response (time to first contact, channel used)

- Initial qualification (phone screen, web chat, SMS conversation)

- Consultation booking rate

- Application start rate

- Application completion rate

- Approval and close rate

Most mortgage teams can tell you their close rate and their monthly application volume. Far fewer can tell you their lead-to-first-contact rate, their consultation booking rate, or how many leads entered their CRM in the last 12 months and were never contacted at all. Those are where the money is.

Step 2: Measure the Numbers at Each Stage

You’re looking for the biggest drop. Pull these numbers from your CRM and your analytics tools:

- Website visitor to lead conversion rate

- Lead to first contact rate (how many leads were reached at all)

- Speed-to-lead (average time from inquiry to first response)

- Consultation booking rate from initial contact

- Application start rate from consultation

- Application completion rate

- Total follow-up attempts per lead (average across your CRM)

When you look at these numbers together, one stage will stand out. That’s where to focus first.

Step 3: Diagnose the Cause

One pattern McKinsey’s research surfaces repeatedly: lenders reach out to customers an average of three times requesting additional documents — and customer satisfaction weakens significantly after the second request. This is a document-friction problem in the mid-funnel. But before you can fix it, you need to know which leak is burning the most revenue.

The four most common causes align directly with the four leaks above:

- Response time over five minutes: infrastructure problem, needs automation

- Low consultation booking rate: qualification or trust problem, needs conversation improvement

- Follow-up depth under three touches: process problem, needs automated sequences

- High CRM backlog of unworked leads: dead database problem, needs reactivation

Step 4: Prioritize the Fix with the Highest ROI

The fastest way to illustrate the potential value of fixing a leak is to look at what it may be costing you right now. If your current lead-to-application rate is 3% and you generate 500 leads a month at $45 average cost per lead, you’re spending $22,500 per month to generate 15 applications.

Moving that rate to 5% could mean 25 applications from the same spend — representing meaningful additional originated revenue per application. These figures are hypothetical and illustrative only. Actual outcomes depend on your lead quality, market, team, and implementation.

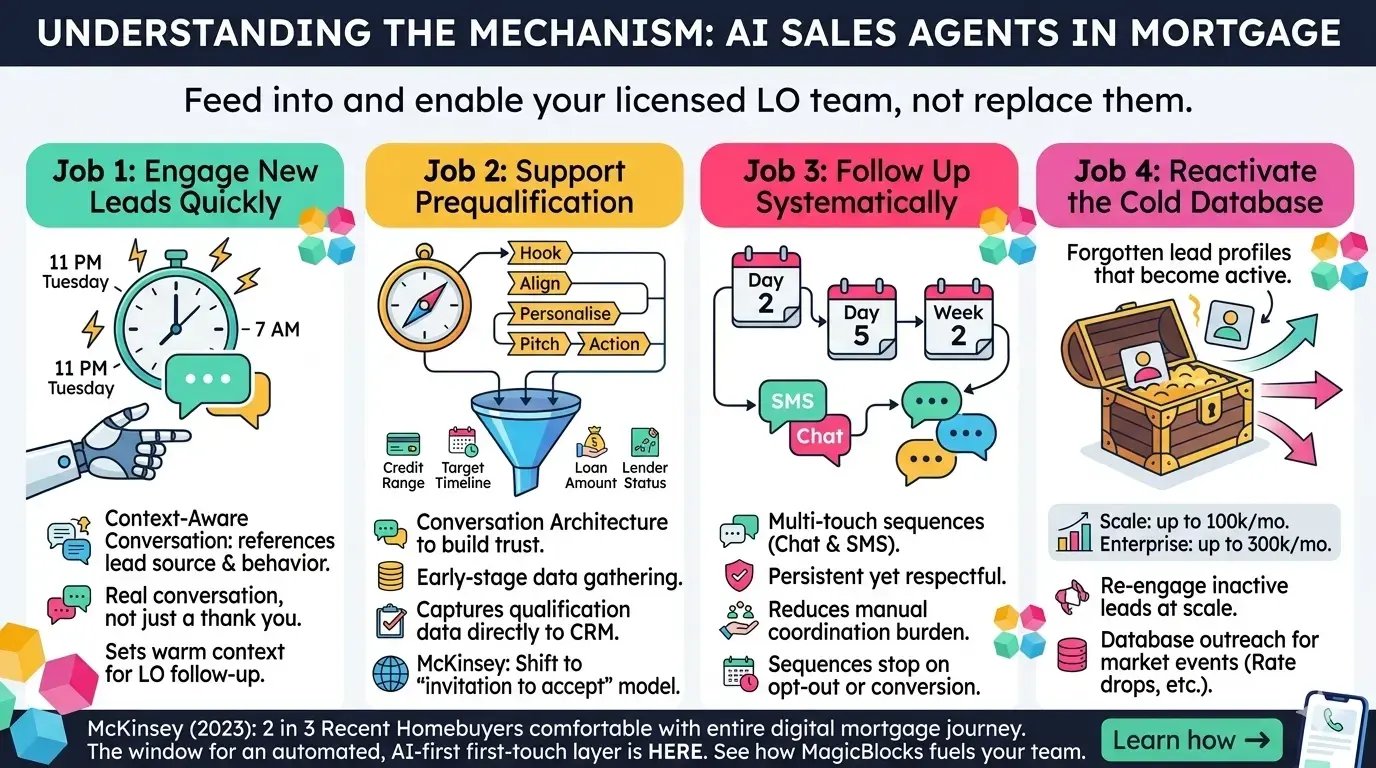

What an AI Sales Agent Actually Does in a Mortgage Funnel

Let’s be specific about the mechanism, because “AI for mortgage” gets used in a lot of ways that mean very different things.

McKinsey’s research found that two in three recent homebuyers are now comfortable completing the entire mortgage journey through digital channels — up from roughly one in three in 2018. Digital adoption in mortgage has passed a structural inflection point. The window to build an automated, AI-first first-touch layer isn’t coming — it’s here.

An AI Sales Agent in the context of mortgage lead conversion supports four distinct functions — all of which feed into and enable your licensed loan officer team, not replace them:

Job 1: Engage New Leads Quickly

The moment a lead submits a form — at 11pm on a Tuesday, during your team’s lunch, at 7am before anyone’s at a desk — an AI Sales Agent can start a real, context-aware conversation. It references where the lead came from, what they were looking at, and what they likely need next. It doesn’t say “Thanks for reaching out, someone will be in touch.” It begins the conversation so your loan officers have warm context when they follow up.

Job 2: Support Prequalification Through Conversation

MagicBlocks agents are built on the HAPPA framework — Hook, Align, Personalise, Pitch, Action — distilled from experience across mortgage, insurance, lending, and related high-intent verticals. This isn’t scripted Q&A. It’s a conversation architecture designed to build trust, capture qualification data, and move the prospect toward a clear next step — all while keeping the interaction natural.

McKinsey highlights that leading lenders are shifting from an “invitation to apply” model to an “invitation to accept” — moving from prequalification to conditional approval delivered via the right channel at the right moment. AI-powered conversation tools can support that shift by handling the early-stage data gathering, allowing loan officers to focus on the consultative work that requires their expertise.

The qualification layer captures credit range, purchase vs. refi intent, target timeline, loan amount, and existing lender status — and feeds it directly into your CRM. All subsequent lending decisions remain with your licensed team. See how the HAPPA conversation framework works in practice.

Job 3: Follow Up Systematically

Leads who don’t respond to the first message aren’t necessarily dead. They need a follow-up cadence that’s persistent enough to catch them when they’re available, but respectful enough that they don’t feel pressured. MagicBlocks agents are designed to execute multi-touch sequences across chat and SMS — immediate, day 2, day 5, week 2, and beyond — reducing the manual coordination burden on your team.

Sequences are designed to stop automatically upon opt-out, conversion, or disqualification. As with all automated outreach, compliance review and appropriate consent practices — including TCPA-compliant opt-in — remain the responsibility of the using organization.

Job 4: Reactivate the Cold Database

Rate drops, new loan programs, FHA limit changes, refinance windows — every market event can be an opportunity to re-engage a prospect who came in 6, 12, or 18 months ago and never completed an application. MagicBlocks agents can support dormant database outreach at scale: the Scale plan handles up to 100,000 inactive lead outreach messages per month, and the Enterprise tier handles 300,000+.

The Digital Channel Shift Mortgage Teams Can’t Ignore

McKinsey’s 2023 research documents a structural shift that’s directly relevant to how mortgage brokers should think about lead conversion. In 2018, around a third of mortgage applicants completed the process entirely digitally. By 2023, that had crossed 50%. And the share of customers who say they’re not comfortable with digital channels has dropped to just 3% — down from 12% five years earlier.

This isn’t a future trend. It’s the current operating environment. And it has a direct implication for lead conversion strategy: a prospect who starts their mortgage journey digitally expects digital engagement to continue. They submitted a web form at 9pm. They’re not waiting by the phone for a loan officer to call them the next morning.

McKinsey also found that 72% of customers now start their loan journey online — with customer demand for digital origination sometimes running twice as high as the actual supply of digital mortgage experiences available to them. That gap between expectation and delivery is where leads disappear.

An AI Sales Agent helps close that gap. It meets the prospect where they are — on the web form, in SMS, in live chat — at the moment of intent, not the next business day.

McKinsey also found that customer satisfaction with loan officers increases with the frequency of interactions during the exploration phase. More well-timed touchpoints tend to produce better outcomes — and this is exactly what automated follow-up sequences are designed to deliver at volume.

Enterprise-Grade Lead Conversion: What Changes at Scale

The audit framework above applies whether you’re a solo broker or a multi-state lending operation. But for enterprise mortgage teams and large brokerages, a few things shift significantly.

Volume and Throughput

An enterprise mortgage operation processing 6,000+ worked leads per month needs infrastructure that doesn’t degrade under volume. MagicBlocks Enterprise is built for this — targeting sub-5-second response times via edge compute across 3,000+ global servers, regardless of simultaneous conversation volume.

The Competitive Stakes at Enterprise Scale

McKinsey’s data on the competitive landscape is direct: purchase-focused nonbanks now account for approximately 32% of purchase origination volumes among the top 50 mortgage lenders, up from 24% in 2018. The gain came primarily at the expense of banks whose response infrastructure — human-first, branch-dependent — couldn’t keep pace with digital-native origination. The lenders that maintained and grew share did so with data, automation, and faster engagement models.

For enterprise lending teams that haven’t yet built that layer, the AI Sales Agent category is where that gap can be addressed — not by replacing loan officers, but by ensuring every lead entering the funnel receives a personalized, timely first engagement before being handed off to your licensed team.

Data Security at Scale

MagicBlocks is SOC 2 Type II certified and aligned with ISO 27001:2022 standards, and is designed to support GDPR compliance for data security and information management.

These certifications address platform security standards and are not mortgage regulatory compliance credentials. They do not cover TCPA, CFPB, RESPA, fair lending, or other lending-specific regulatory requirements. Regulated lending teams should conduct their own compliance assessment with qualified legal counsel.

Security and compliance documentation is available at trust.magicblocks.ai.

For enterprise customers, outbound messages pass through the Guardian Engine — a configurable review layer that applies messaging policies such as TCPA and DNC safeguards, quiet hour rules, opt-out handling, and PII protections based on customer-defined data and rules.

This system is designed to help reduce the risk of non-compliant messaging. Final compliance responsibility, including maintaining appropriate consent records, remains with the licensed organization conducting the outreach.

Multi-Team and Multi-Branch Operations

Enterprise mortgage groups operate across branches, under multiple brand flags, with loan officers distributed across regions. MagicBlocks handles this through workspace management — each branch or team runs its own AI Sales Agent configurations, playbooks, and conversation sequences, while the overall operation maintains consistent data governance and brand standards. Agency workspaces are available on Scale and Enterprise plans.

CRM Integration and Data Governance

At enterprise scale, leads aren’t just conversations — they’re data assets that need to flow cleanly into existing systems. MagicBlocks integrates with Salesforce, HubSpot, GoHighLevel, and other CRMs via Zapier and REST API, pushing structured qualification data from every conversation into the right place at the right time. No manual data entry. No CRM contamination from AI conversations.

What the Numbers Look Like in Practice

Beeline, an online mortgage lender, deployed an AI Sales Agent as its primary lead engagement layer. According to results published by CEO Nick Liuzza in a NASDAQ shareholder letter, the deployment produced a 737% increase in completed applications, 484% growth in qualified leads, and a 48.72% conversation-to-lead conversion rate, with monthly origination reaching $30M within six months of deployment.

These results reflect a single enterprise-scale deployment under specific market and operational conditions. Individual results will vary based on lead volume, market environment, team configuration, and implementation approach.

The methodology developed during that deployment is encoded into the MagicBlocks HAPPA framework. The Beeline case study reflects a specific implementation under conditions that may differ from other organizations’ environments, and results from other deployments will vary.

Read the full Beeline case study.

Mortgage Lead Conversion Trends in 2026

The structural shift happening in mortgage sales right now is a compression of the human sales team’s role in top-of-funnel volume work. The rote work — responding quickly, supporting initial prequalification, following up consistently, reactivating cold leads — can increasingly be supported by automation.

Loan officers who previously spent significant time on initial outreach and qualification can be freed to focus on complex consultations, relationship management, and the parts of the sale that require human judgment — and that require a licensed professional.

McKinsey’s research on the broker market adds a useful frame: one in four borrowers consider a lender their real estate agent recommended, and agents recommend nonbank lenders twice as often as they recommend banks — specifically because of their reputation for faster processing and more knowledgeable loan officers. The competitive advantage nonbanks hold isn’t a product advantage. It’s an operational one. AI Sales Agents are one of the primary mechanisms for scaling that operational advantage — handling the volume, speed, and consistency challenges that human teams alone can’t sustain at scale.

In MagicBlocks customer deployments, teams have reported observations such as AI agents handling a significant share of first-touch engagement, faster delivery of qualification data to loan officer desks, increased follow-up depth per lead, and re-engagement activity on dormant lead databases.

These are aggregate observations across a subset of MagicBlocks customers and are not guarantees of performance. Individual results vary based on industry segment, lead source, team configuration, and deployment approach.

The brokers and lending operations improving conversion in 2026 aren’t necessarily the ones with the most loan officers. They’re the ones that have addressed the four leaks — and the way many are doing it is by deploying AI Sales Agents as the first layer of their funnel, with their licensed teams focused on the conversations that matter most.

Running the Audit: Solo Broker vs. Enterprise Operation

For Independent Mortgage Brokers and Solo Loan Officers

Your biggest leak is likely response time and follow-up depth. You’re one person — or a small team — and you physically can’t respond to every lead within minutes, especially outside business hours. Deploying an AI Sales Agent as your first responder can help address this. Every new inquiry can receive a context-aware response quickly. Every lead can receive systematic follow-up automatically. You can show up to work with qualified conversations already in progress.

Create your AI Sales Agent at magicblocks.ai.

For Mortgage Branch Managers and Multi-State Brokerages

Your leaks are more structural. You’ve got inconsistent follow-up across a team where different loan officers work leads differently, a CRM backlog growing every quarter, and the compliance considerations of outbound AI communications at scale. The audit process is the same — map your funnel, measure the drop-off points, prioritize the biggest leak — but the fix needs to work across your entire operation, not just one LO’s workflow.

MagicBlocks Scale and Enterprise plans are designed for this. The Dynamic Journey Engine computes the next best action in real time across every active lead conversation simultaneously, without requiring your team to build or maintain workflow diagrams. The Guardian Engine provides an automated review layer on every outbound message. Your loan officers get structured qualification data. Your CRM gets clean records.

Frequently Asked Questions

Why do mortgage brokers lose leads even when they have a full team?

The most common cause isn’t a team problem — it’s a timing problem. Research shows contact rates drop significantly after the first few minutes following a lead inquiry. Most teams can’t consistently respond within that window, especially outside business hours. The leads don’t disappear because the team is bad. They disappear because the gap between inquiry and first contact is too long for the prospect to wait.

Where in the mortgage funnel do leads most commonly drop off?

There are five high-risk stages: the web form (technical friction, slow load, poor mobile experience), the first response window (speed-to-lead), the initial qualification conversation (trust and clarity), the consultation booking (friction and urgency), and the application (form length and complexity). Most brokerages have significant leakage at two or three of these simultaneously.

What’s the ideal response time for a new mortgage lead?

Under five minutes substantially improves contact rates compared to longer delays. Under 60 seconds — which is what an AI Sales Agent is designed to deliver — is where many teams see meaningful conversion improvement. At that speed, the prospect is still in the mindset that prompted the inquiry. Individual results will vary.

How do AI Sales Agents support TCPA and DNC compliance in mortgage outreach?

MagicBlocks routes every outbound message through the Guardian Engine before it sends — an automated review layer designed to check against TCPA guidelines, quiet hours, DNC list status, opt-out records, and PII standards. This is designed to help reduce the risk of non-compliant messages. Organizations remain responsible for maintaining appropriate consent records, configuring outreach settings correctly, and conducting their own legal review of outbound messaging practices. For enterprise teams, MagicBlocks carries SOC 2 and ISO 27001 data security certifications; these are not regulatory compliance certifications for mortgage lending.

Can an AI Sales Agent work a dead CRM database of old mortgage leads?

Yes. Database reactivation is one of the core functions MagicBlocks AI agents are designed to support. The system can send personalized outreach to dormant leads — triggered by rate changes, new loan programs, or time-based cadences — and surface the ones who are ready to re-engage. A meaningful share of properly worked dormant leads can re-engage with the right outreach, though engagement rates vary significantly based on lead age, outreach cadence, message relevance, and market conditions.

Is MagicBlocks only for small mortgage brokerages?

No. MagicBlocks is deployed by enterprise lending teams processing thousands of leads per month. The Enterprise tier starts at $15,000/month and handles 6,000+ worked leads, 300,000 inactive lead outreach messages, and 40,000 web chats per month. It includes SOC 2 and ISO 27001 data security certifications, multi-workspace support for multi-branch operations, and dedicated expert configuration support.

What kind of conversion improvement might fixing lead leakage produce?

Results vary significantly by organization, market, and implementation. The Beeline case study — a single enterprise-scale deployment — produced 737% more completed applications and 484% growth in qualified leads, per the Beeline CEO’s NASDAQ shareholder letter. Individual results will vary and the Beeline outcomes should not be interpreted as typical or expected results. Some organizations have reported meaningful improvements in lead-to-application rates after implementing faster response and automated follow-up — but outcomes depend on lead quality, team configuration, market conditions, and how the platform is deployed.

How does the shift to digital channels affect mortgage lead conversion strategy?

Significantly. McKinsey found that more than half of 2023 mortgage applicants completed the entire process through a lender’s website or mobile app — up from roughly a third in 2018. And only 3% of borrowers today say they’re uncomfortable with digital channels. That means the large majority of your leads expect digital-first engagement. If your first response is a phone call 20 minutes after form submission, you’ve already fallen short of the experience they expected — regardless of your rate.

Stop Losing Revenue You Already Paid For

Every lead your team doesn’t reach quickly, every follow-up sequence that stops after one touch, every dormant CRM record that hasn’t been re-engaged — that’s revenue you already spent money to acquire, sitting in a funnel that isn’t converting it.

McKinsey’s research is clear that the mortgage market’s next competitive frontier is the conversion layer — the gap between initial expression of interest and completed application.

The lenders closing that gap faster, with more personalized engagement and smarter qualification, are the ones taking share from slower-moving incumbents. AI Sales Agents — deployed as a support layer for licensed loan officer teams — are among the primary tools being used to do it.

MagicBlocks deploys AI Sales Agents designed to help address all four leaks: slow response, inconsistent qualification support, insufficient follow-up depth, and dormant databases. They work every lead at every stage, around the clock — without adding headcount, with built-in automated compliance controls, and with structured data flowing directly to your licensed team.

This content is intended for licensed mortgage professionals. It does not constitute financial, legal, or regulatory advice. All performance figures cited are client-specific and subject to results-may-vary qualifiers noted throughout. Organizations should conduct their own compliance review with qualified legal counsel before deploying AI-powered outreach tools.

Want to see this in action?

See a demoRead the playbook. Now see it run.

Watch a 4-minute demo. No sales pitch. Then decide if you want to talk.