How AI Sales Agents Increase Mortgage Lead Conversion by 6X

These figures were disclosed in a public shareholder letter, lending them a level of accountability unusual for marketing claims. They reflect Beeline's specific deployment, traffic mix, and internal baseline.

Discover how AI sales agents like Beeline's Bob dramatically increase mortgage lead conversion rates with instant responses and personalized engagement. Learn to replicate this success in your own sales funnel.

On this page 10

- The Mortgage Lead Problem Nobody Wants to Admit

- Why Mortgage Companies Are Moving Toward AI-First Sales Models

- Meet Bob: The AI Sales Agent Behind Beeline’s 6X Results****Beeline AI Sales Agent Driving 6x Mortgage Lead Conversion

- How AI Sales Agents Increase Mortgage Lead Conversion

- The HAPPA Framework: Why Some AI Agents Sell Better Than Others

- The Numbers: Beeline’s Results by the Metric

- Emotional Intelligence in Mortgage AI Conversations

- How to Replicate the Beeline Model in Your Mortgage Funnel

- Common Mistakes When Implementing AI Sales Agents in Mortgage

- Frequently Asked Questions

In January 2026, Beeline Holdings CEO Nick Liuzza published a shareholder letter to NASDAQ investors disclosing that Bob, Beeline’s AI sales agent built on MagicBlocks, generated six times higher lead conversion rates and eight times more completed mortgage applications on their web chat channel, compared to Beeline’s own previous human-led chat benchmarks — without incremental operational cost.

These figures were disclosed in a public shareholder letter, lending them a level of accountability unusual for marketing claims. They reflect Beeline’s specific deployment, traffic mix, and internal baseline. Results for other lenders will vary based on their own lead volume, market, and implementation.

It came from an AI agent that responded in under five seconds, worked around the clock, and guided borrowers through a structured sales conversation before a single loan officer got involved.

The data behind this shift is consistent across the industry. McKinsey research on AI-enabled mortgage ecosystems found that one bank’s AI homebuying platform now drives over 30% of total mortgage origination, and US lenders with integrated digital experiences see twice the customer satisfaction gains of conventional players.

HBR identifies personalized, real-time engagement as the defining competitive advantage in high-stakes financial decisions, and Gartner projects that by 2027, 95% of seller outreach workflows will begin with AI, up from less than 20% in 2024.

The window for early adoption advantage is open right now. This article breaks down exactly how Beeline achieved a 6x conversion lift, the mechanics that made it work, and how mortgage lenders and brokers can replicate the model in their own funnels.

What You’ll Learn

- The mortgage lead problem nobody wants to admit

- Why mortgage companies are moving toward AI-first sales models

- Meet Bob: the AI sales agent behind Beeline’s 6x results

- How AI sales agents increase mortgage lead conversion

- The HAPPA Framework: why some AI agents sell better than others

- Beeline’s results by the metric

- Emotional intelligence in mortgage AI conversations

- How to replicate the Beeline model in your mortgage funnel

- Common mistakes when implementing AI sales agents

The Mortgage Lead Problem Nobody Wants to Admit

Mortgage companies spend enormous sums generating leads. The average cost per mortgage lead ranges from $20 to over $200 depending on channel.

And yet, for most lenders and brokers, the majority of those leads never convert. Not because the borrowers weren’t serious. Because nobody responded fast enough, or at all.

This isn’t a hypothetical problem. It’s a documented, industry-wide failure that plays out thousands of times a day.

Why 60% of Mortgage Leads Arrive After Business Hours

Modern borrowers research mortgages on their own schedule. They scroll rates at 11pm. They compare lenders on a Sunday afternoon. They submit inquiries when the thought strikes them, which statistically is most often outside the 9-to-5 window.

Beeline’s own data confirmed that 60% of their mortgage inquiries arrived after business hours. For a team-dependent model, that’s 60% of your lead flow landing in a void.

By the time a loan officer sees that inquiry the next morning, the borrower has already filled out two more forms with competitors. One of them responded. And that conversation is already underway.

The Speed-to-Lead Gap

InsideSales.com’s 2021 study covering over 55 million sales activities across 400+ companies found significantly higher qualification rates when leads were contacted within 5 minutes compared to a 30-minute delay. Speed-to-lead research consistently supports the value of rapid response — though the specific multipliers vary by industry, lead source, and methodology. For mortgage specifically, the principle holds: borrowers researching multiple lenders simultaneously are more likely to engage with the first respondent.

That is the gap. Most mortgage businesses are losing deals not because they lack good products or competitive rates, but because they are simply too slow.

Harvard Business Review’s research on the customer decision journey reinforces why this matters so deeply in mortgage: the window of peak buying intent is narrow and closes fast. Borrowers who don’t get an immediate response don’t wait. They shift their attention, and with it, their trust.

Why Sales Teams Chase the Wrong Leads

McKinsey’s 2025 research on agentic AI in banking found that relationship managers at many financial institutions spend a relatively small proportion of their working time in direct client dialogue — with the majority going to administrative tasks, lead sorting, and compliance-related work.

The specific figures vary by institution and role type. For mortgage loan officers, the principle applies: reducing time spent on administrative follow-up and unqualified leads is a meaningful productivity lever.

Without intelligent qualification, sales teams default to working the loudest leads, not the best ones. The result is a funnel that produces a lot of activity and very little revenue.

Low Engagement Rates

Even borrowers who engage with a lender’s website often leave without a meaningful interaction. Standard contact forms convert poorly. Static FAQs don’t address the specific concerns of a first-time buyer at 11pm who isn’t sure if their credit score qualifies. The funnel leaks at every stage.

Research across multiple industries suggests that first-responder advantage is significant — with some studies attributing a meaningful share of closed business to the vendor who makes initial contact. In mortgage, where borrowers often research multiple lenders simultaneously, speed of first response is widely cited as a conversion factor. The degree of advantage varies by lead source, borrower intent, and competitive density in your market.

Why Mortgage Companies Are Moving Toward AI-First Sales Models

Mortgage is uniquely suited to AI-driven sales automation. Not because it’s simple, but because of the specific combination of factors that make the category so hard to serve well with traditional teams: high lead volumes, multi-step decision processes, extreme price sensitivity, and a borrower psychology defined by anxiety and high stakes.

Why Mortgage Is a High-Hesitation Purchase

Buying a home is the largest financial transaction most people will ever make. Harvard Business Review’s research on customer experience in financial services establishes that competitive advantage in this category is no longer primarily about product or price.

It’s about the ability to deliver personalized experiences that build trust across the entire decision journey. Borrowers who feel understood and guided are dramatically more likely to complete an application.

This is also why the old model, generating a lead, adding it to a CRM, and waiting for a callback, fails so consistently. The emotional peak of the borrower’s decision window doesn’t align with business hours. When a borrower is ready to engage, they want to engage now.

The Economics of AI vs. SDR Teams

A 2024 McKinsey report on AI in lending found that a majority of financial institutions surveyed reported measurable cost reductions and productivity gains in their lending operations after AI implementation. Some institutions using AI-driven engagement systems have reported pipeline growth and revenue improvements — though the magnitude varies by institution, implementation type, and market. These figures reflect survey-reported outcomes across diverse banking contexts, not mortgage-specific projections.

One commercial bank found that AI-assisted lead prioritization achieved twice the conversion rate of traditional approaches.

The math is straightforward. A human SDR team capable of responding within five minutes, around the clock, seven days a week, at meaningful scale requires enormous headcount investment. An AI sales agent does the same job consistently, without burnout, error, or variability, at a fraction of the cost.

How AI Changes the Mortgage Funnel

McKinsey’s research on AI-enabled housing ecosystems found that a multinational European bank’s AI-enabled homebuying app now accounts for more than 30% of the bank’s total mortgage origination.

A leading Asia-Pacific bank’s AI-powered home financial planner generates about 25% of the bank’s mortgage leads. Among leading US financial players offering integrated digital experiences, customer satisfaction improvements run at twice the rate of institutions using conventional models.

The pattern is consistent: mortgage businesses that move AI into the front of the funnel, making it the first point of contact rather than an afterthought, see dramatically different conversion outcomes. The funnel doesn’t just get faster. It gets smarter.

MagicBlocks is built specifically for this shift. Its AI sales agents respond immediately to mortgage leads, qualify borrowers through structured conversation, and create the kind of engagement that moves a prospect from inquiry to application automatically.

Meet Bob: The AI Sales Agent Behind Beeline’s 6X Results****Beeline AI Sales Agent Driving 6x Mortgage Lead Conversion

In CEO Nick Liuzza’s January 2026 shareholder letter to Beeline Holdings (NASDAQ: BLNE) investors, he highlighted Bob, the AI chat and production agent at the center of Beeline’s AI strategy, as generating six times higher lead conversion rates and eight times more mortgage applications than internal benchmarks, without incremental operational cost.

That disclosure appeared in a public shareholder letter. Not a marketing case study. A performance disclosure to public market investors, one of the most credible contexts in which a company can make claims about its own technology.

Bob isn’t a chatbot in the traditional sense. He doesn’t present a menu of options and wait for a borrower to click through. He starts a real conversation, reads the borrower’s situation, qualifies their intent, and moves them toward an application the same way a great loan officer would, if that loan officer never slept, never lost focus, and could handle thousands of conversations simultaneously.

Sub-5-Second Response Time

Bob responds to mortgage inquiries in under 5 seconds. That single capability is one of the most powerful conversion levers in the category.

Research consistently shows that leads contacted within the first minute see up to 391% higher conversion rates. In Beeline’s deployment, leads contacted within 5 seconds showed significantly higher conversion rates compared to slower response times consistent with broader speed-to-lead research. The specific multiplier reflects Beeline’s lead mix and market context. The principle that faster initial response correlates with higher engagement is well-supported, though the magnitude of improvement will vary by lender.

The 2am homebuyer who fills out an inquiry form and receives an immediate, intelligent response from Bob doesn’t experience a dead end. They experience a conversation. That shift in experience is where the 6x conversion difference lives.

24/7 Mortgage Lead Engagement

For Beeline, 60% of their inquiries arrived outside business hours. Bob doesn’t have office hours. He’s available around the clock, engaging borrowers with the same quality of conversation at midnight that a loan officer would deliver at 10am, and faster, at unlimited scale.

A 2025 survey found that a growing share of homebuyers report using AI tools in their mortgage research process. These figures reflect self-reported survey responses and vary by methodology and sample — but they point to increasing borrower comfort with AI-assisted interactions in the mortgage journey.

Borrowers aren’t just comfortable with AI interactions. They’re actively using them to make decisions. An AI agent that shows up first with a great experience wins that comparison every time.

Personality-Driven Conversations

One of the most commercially important things about Bob is that he doesn’t sound like a bot. He oozes personality.

He’s warm, clear, and contextually aware. When a borrower says they’re stressed about their credit situation, Bob doesn’t pivot to a product pitch.

He acknowledges the anxiety, validates the concern, and redirects to a realistic next step. That emotional responsiveness, delivered consistently at scale, is what turns a conversation into a qualified lead.

Conversational Memory

Bob remembers. If a borrower interacted with Beeline’s site last week and comes back today, Bob picks up where they left off. He doesn’t ask for the same information twice.

He doesn’t start from scratch. This continuity is what transforms an AI interaction from a transaction into a relationship. McKinsey’s personalization research found that 71% of consumers expect companies to deliver personalized interactions, and 76% get frustrated when that doesn’t happen.

Bob gets this balance right because the personalization is driven by actual conversation context, not just profile data.

Compliance-Safe AI Design

Mortgage is one of the most heavily regulated industries in the US financial system.

CFPB oversight, TCPA requirements, fair lending laws, the compliance stakes are real. Bob operates within MagicBlocks’ Guardian Engine, a built-in guardrail layer designed to keep conversations within defined topic boundaries, enforce required disclosures, and trigger human escalation when needed. This architecture supports compliance workflows — though regulatory compliance ultimately depends on the deploying organization’s configuration, legal counsel, and operational oversight. Beeline’s deployment demonstrated that AI-assisted engagement and responsible design can coexist effectively.

How AI Sales Agents Increase Mortgage Lead Conversion

The 6x conversion improvement Beeline achieved with Bob wasn’t the result of a single capability. It was the cumulative effect of five distinct mechanisms working together.

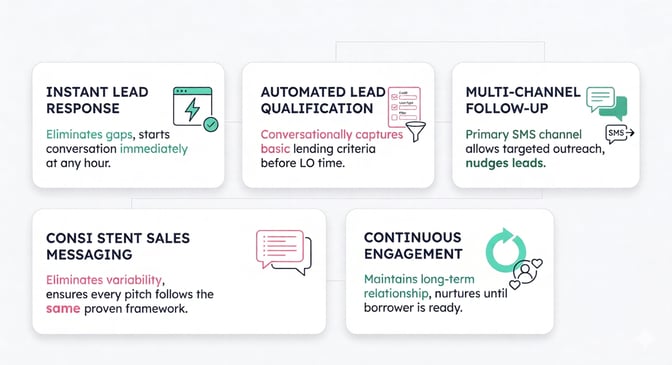

1. Instant Lead Response

Every second a mortgage lead goes unanswered is a second the borrower is considering alternatives.

AI sales agents eliminate that gap entirely. The moment a borrower submits an inquiry, at any hour, the conversation starts. No queue. No wait. No morning email from a loan officer who missed the window.

This first-contact advantage is the highest-impact lever in mortgage conversion. It doesn’t require better marketing, a lower rate, or a better product. It requires being there first, with something worth responding to.

2. Automated Lead Qualification

Not every inquiry is a qualified buyer. AI agents can determine, through structured conversation, whether a borrower meets basic lending criteria before a loan officer’s time is ever invested.

Credit score range, loan type, property value, purchase timeline: these can all be captured conversationally and naturally, without the interaction feeling like a form.

The result is a sales team that only ever sees warm, qualified leads. Conversion rates go up. SDR time goes down. Cost per acquired loan drops dramatically.

3. Multi-Channel Follow-Up

A single missed response doesn’t have to be the end of the opportunity.

MagicBlocks currently supports SMS as the primary follow-up channel, allowing loan officers to re-engage leads manually through targeted outreach after an initial AI conversation.

A borrower who went quiet after a chat session can receive an SMS follow-up timed to their journey stage. A lead who never completed the qualification flow can get a nudge at the right moment.

The channel is focused, the data from the AI conversation travels with it, and the handoff is clean. As AI-led engagement matures across the industry, the case for expanding channel coverage only strengthens: Gartner projects that 95% of seller outreach workflows will begin with AI by 2027, making the infrastructure for fast, intelligent follow-up a baseline expectation rather than a differentiator.

4. Consistent Sales Messaging

Human sales teams have good days and bad days. Individual loan officers vary in how they handle objections, position products, and follow the qualification script.

AI agents are perfectly consistent. Every borrower gets the same quality of conversation. Every pitch follows the same proven framework. There’s no variability from rep to rep, no message drift, no off-brand interaction.

5. Continuous Engagement

Mortgage decisions don’t happen overnight. A borrower who inquires today might not be ready to apply for three months.

AI agents can maintain that relationship automatically, checking in at the right intervals, surfacing relevant content, and keeping the lender top-of-mind until the borrower is ready to move. This long-term nurturing capacity is structurally impossible for a human team to deliver at scale.

MagicBlocks enables teams to design structured AI sales conversations that cover all five of these mechanisms, from first contact through qualification, follow-up, and reactivation, without requiring a full engineering team to implement.

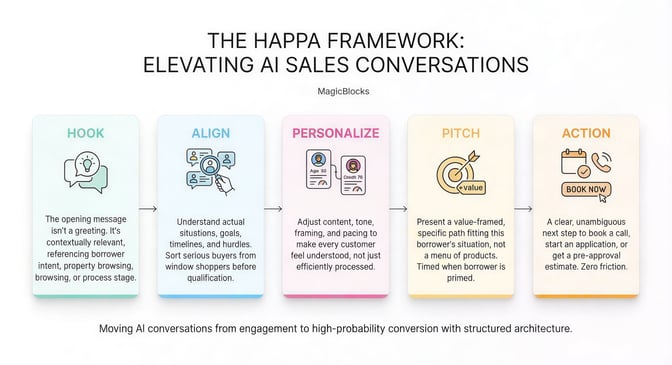

The HAPPA Framework: Why Some AI Agents Sell Better Than Others

Not all AI sales agents are built the same. The difference between an agent that feels like a FAQ page and one that converts like a top-performing loan officer comes down to the conversation architecture underneath it.

MagicBlocks’ HAPPA Framework — developed through the MagicBlocks team’s prior experience across lead generation work in mortgage and other high-ticket industries — structures AI conversations around proven sales psychology principles.

HAPPA stands for Hook, Align, Personalize, Pitch, Action. Each stage serves a distinct conversion function.

Hook

The opening message isn’t a greeting. It’s a conversion lever. Bob doesn’t say ‘Hi, how can I help you?’ He says something contextually relevant, referencing what the borrower was looking at, what stage of the process they appear to be in, or what their likely intent is.

A first-time buyer browsing 30-year fixed rates gets a different hook than a repeat buyer comparing refinance options.

Context-aware hooks dramatically increase the probability that a borrower responds. A generic greeting gets ignored. A relevant opener gets a reply. And a reply is the beginning of a conversion.

Align

Before any product is mentioned, Bob works to understand the borrower’s actual situation. What are they trying to accomplish? What’s their timeline? What’s holding them back? This alignment stage separates serious buyers from window shoppers, and it does it through conversation, not interrogation.

This also means the sales team never gets handed an unqualified lead. The AI does the sorting before a human loan officer gets involved.

Personalize

A first-time homebuyer in their 30s with a 640 credit score has a fundamentally different set of concerns than a seasoned investor refinancing a third property.

Bob adjusts not just the content of what he says, but the tone, framing, and pacing of the conversation. HBR identifies this as the new competitive battleground in financial services: the ability to make every customer feel genuinely understood, not just efficiently processed.

Pitch

When the time is right, Bob presents the relevant option. Not a menu of every product Beeline offers, but the specific path that fits this borrower’s situation. ‘Based on what you’ve shared about your goals and timeline, here’s the loan type that may be worth exploring with one of our loan officers’.

Note: Any AI-generated messaging that references specific financial savings or recommends a specific loan product should be reviewed by a licensed loan officer before deployment. AI agents should facilitate conversations and qualify intent — loan product recommendations should be made by licensed professionals.

Action

Every HAPPA conversation ends with a clear next step. Book a call with a loan officer. Start an application. Get a pre-approval estimate. There’s no ambiguity about what happens next, and there’s no friction in getting there. The AI has done the qualification work. The loan officer just needs to show up for the conversation that matters.

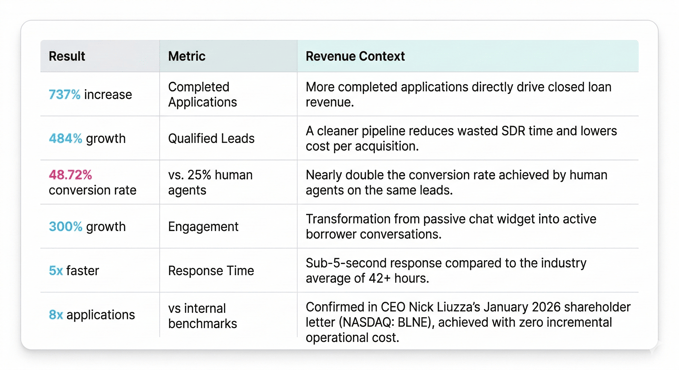

The Numbers: Beeline’s Results by the Metric

Beeline’s results with Bob are drawn from two primary sources: the detailed performance metrics published in the MagicBlocks Beeline case study (737%, 484%, 48.72%, 300%), and the 6x lead conversion and 8x applications figures confirmed independently in CEO Nick Liuzza’s January 2026 shareholder letter to NASDAQ investors. Here’s what each metric means in revenue terms.

The headline figure, 8x mortgage applications against internal benchmarks with no incremental operational cost, is what makes this case study particularly significant.

It demonstrates that AI-driven lead conversion isn’t just about doing the same thing faster. It’s about achieving outcomes that weren’t possible with a team-dependent model.

McKinsey’s early agentic AI pilots in financial services have documented two- to threefold increases in qualified leads in some implementations. Beeline’s 484% growth in qualified leads measured against their own internal baseline over their deployment period — represents a strong outcome for their specific context. As with all single-client results, this figure reflects Beeline’s particular lead mix, market, and configuration and should not be interpreted as a projection for other deployments.

Emotional Intelligence in Mortgage AI Conversations

Mortgage decisions are emotionally significant. A borrower who’s worried about qualifying, stressed about their credit, or anxious about timing doesn’t want an efficient transaction.

They want to feel like someone understands what’s at stake for them. This is where most AI implementations fail, and where Bob consistently didn’t.

Supporting Financially Stressed Borrowers

When a borrower told Bob they were concerned about their credit score, he didn’t pivot to a disclaimer.

He acknowledged the concern, validated the stress, and redirected to a realistic next step, connecting them with a licensed loan guide who could provide tailored guidance.

That response, empathetic, accurate, and actionable, is what the case study describes as going beyond automation to deliver genuine emotional support.

This matters commercially. A borrower who feels dismissed or misunderstood at the first point of contact doesn’t apply. A borrower who feels seen and guided does.

Turning Conversations Into Relationships

Nick Liuzza captured it precisely: the goal was to meet each lead at the right moment, with a defined journey from inquiry to application. Bob wasn’t the endpoint of the process.

He was the beginning of a relationship, one that warmed a lead, built initial trust, and handed a prepared, qualified borrower to the loan officer team. HBR’s research on customer experience in financial services identifies ‘intelligent experience engines’ as the defining capability of companies that win on customer experience, systems that assemble high-quality, personalized interactions at a scale previously impossible with human-only teams.

Why Warmth Converts Better Than Efficiency Alone

There’s a version of AI deployment that prioritizes efficiency above everything else: faster qualification, leaner scripts, fewer messages. That version doesn’t produce results like Beeline’s.

What produces those results is an agent that combines operational precision with genuine warmth, one that moves fast and still makes the borrower feel like they matter.

The 48.72% conversation-to-lead conversion rate Bob achieved versus 25% for human agents on the same lead pool reflects this directly. It’s not that Bob was more efficient. It’s that he was better at making borrowers feel confident enough to move forward.

How to Replicate the Beeline Model in Your Mortgage Funnel

Beeline’s results demonstrate what AI-assisted lead engagement can achieve in a mortgage context when implemented with structured conversation design, clear qualification logic, and compliance guardrails. The underlying approach — instant engagement, automated qualification, structured sales framework — is available to mortgage brokers, independent lenders, and agencies regardless of size.

Actual results will depend on your lead volume, traffic sources, agent configuration, market conditions, and team follow-up process. Beeline’s specific figures should not be interpreted as a projection of what your deployment will achieve.

What You Need to Deploy an AI Sales Agent

The core requirements are simpler than most teams expect. You need a lead source that routes new inquiries into the AI system in real time, a conversation framework built around your specific borrower types and products, and a CRM integration that allows qualified leads to flow directly to loan officers without manual intervention.

MagicBlocks handles the conversation architecture and CRM connectivity. Teams that deploy with an existing GoHighLevel setup, HubSpot instance, or Twilio SMS pipeline can have an AI agent live on their mortgage funnel with minimal engineering overhead.

Mortgage-Specific Agent Design

The Beeline model works because Bob was built for mortgage borrowers, not adapted from a generic template. The conversation logic follows a consultative, educational, and emotionally resonant arc that fits how mortgage decisions actually get made. A first-time buyer needs different language than a refinancing homeowner. A borrower with a 580 credit score needs different guidance than one with a 720.

MagicBlocks’ mortgage-specific templates encode this logic from the start, built on the HAPPA framework and informed by the same $200M+ in conversion experience that shaped Bob.

Key Borrower Data to Capture

- Credit score range (above or below 580, 620, 680 thresholds)

- Loan type intent (purchase, refinance, cash-out, FHA, VA)

- Purchase timeline (immediate, 3 months, 6 or more months)

- Property value and location (for product eligibility)

- First-time buyer status (determines which programs apply)

Integrating AI With Mortgage CRMs

The AI agent isn’t a standalone tool. It’s the front end of a lead conversion system. Once a borrower is qualified through conversation, that lead with all the data collected should flow directly into your CRM, trigger a notification to the assigned loan officer, and create a follow-up task or appointment. MagicBlocks integrates natively with GoHighLevel, HubSpot, Twilio, and Calendly, making this handoff seamless.

Common Mistakes When Implementing AI Sales Agents in Mortgage

Over-Automation

AI agents should start the conversation, not own it entirely. The most effective deployments use AI to qualify and warm leads, then hand off to a human loan officer for the relationship-intensive close. Removing human judgment from the high-stakes conversations at the bottom of the funnel is where over-automation goes wrong.

Poor Qualification Logic

An AI agent that asks the wrong questions, or asks them in the wrong order, surfaces unqualified leads. The qualification logic needs to be built around your actual lending criteria, not a generic template. Credit thresholds, loan type eligibility, and timeline compatibility all need to be encoded into the conversation design.

Generic AI Messaging

A mortgage borrower who gets a response that could have come from any lender in the country doesn’t convert. The agent needs to sound like your brand, know your products, and understand the specific borrower types you serve. Generic AI messaging is the fastest way to replicate the experience of a bad chatbot, which is worse than no chatbot at all.

Lack of CRM Integration

AI-captured lead data that lives in a separate system and requires manual transfer is a bottleneck that kills conversion speed. The entire point of AI qualification is to get clean, organized lead data to a loan officer faster. If that data doesn’t flow automatically into your CRM and trigger a workflow, you’ve eliminated the conversion advantage.

Ignoring Compliance Considerations

Mortgage AI agents operating without compliance guardrails expose lenders to serious regulatory risk. TCPA compliance for SMS, CFPB disclosure requirements, and fair lending obligations all apply to AI-driven interactions. MagicBlocks’ Guardian Engine provides guardrail infrastructure designed to reduce the risk of non-compliant AI interactions — including topic restrictions, disclosure prompts, and escalation triggers. Deploying organizations remain responsible for configuring these guardrails appropriately and maintaining oversight of AI-driven conversations in line with their own regulatory obligations and legal counsel’s guidance.

Frequently Asked Questions

How do AI sales agents increase mortgage lead conversion?

AI sales agents increase mortgage lead conversion by responding to inquiries instantly, qualifying borrowers automatically through structured conversation, and maintaining consistent follow-up across every hour of the day.

The primary drivers are speed-to-lead (response within seconds rather than hours), 24/7 coverage, and intelligent qualification that filters serious buyers before human team time is invested.

What results did Beeline achieve using AI sales agents?

Beeline achieved a 737% increase in completed mortgage applications, 484% growth in qualified leads, a 48.72% conversation-to-lead conversion rate versus 25% with human agents, 300% growth in engagement, and 5x faster response times.

CEO Nick Liuzza’s January 2026 shareholder letter confirmed that Bob generated six times higher lead conversion and eight times more applications than internal benchmarks, without incremental operational cost.

What is speed-to-lead in mortgage marketing?

Speed-to-lead is the time between a borrower submitting an inquiry and the first response from the lender or broker. Research consistently shows that responding within 5 minutes produces 21x higher qualification rates than waiting 30 minutes.

For mortgage, where borrowers are often researching multiple lenders simultaneously, being first to respond is frequently the single most important conversion factor.

Can AI agents qualify mortgage borrowers automatically?

Yes. AI sales agents can collect credit score range, loan type intent, purchase timeline, property details, and first-time buyer status through natural conversation, without the interaction feeling like a form.

This qualification data flows directly into the CRM, allowing loan officers to prioritize their time on the borrowers most likely to convert.

Are AI sales agents compliant with mortgage regulations?

MagicBlocks’ Guardian Engine includes built-in guardrails designed to support CFPB-aligned disclosures, TCPA-aligned SMS workflows, and fair lending principles — including topic restrictions and human escalation triggers. These features are designed to reduce compliance risk, but they are not a substitute for legal counsel or a guarantee of regulatory compliance. Deploying organizations remain responsible for their own compliance obligations. Beeline’s deployment in the US mortgage market demonstrates that AI-assisted engagement and responsible design can be implemented together effectively.

How quickly do AI agents respond to mortgage inquiries?

MagicBlocks AI agents respond in under 5 seconds via edge compute infrastructure. Bob’s sub-5-second response time was central to Beeline’s conversion results.

The case study confirmed that leads contacted within 5 seconds were 5x more likely to convert, compared to the industry average response time of 42+ hours.

What is the difference between a chatbot and an AI sales agent?

A chatbot follows a scripted decision tree. It presents options and waits for the user to click. An AI sales agent has conversational intelligence.

It reads the borrower’s intent, adapts its responses based on context, handles objections, remembers prior interactions, and drives toward a specific outcome such as a booked call, a completed application, or a qualified lead handoff.

The performance difference can be substantial: Bob converted 48.72% of conversations into leads in Beeline’s deployment — compared to 25% for human agents on the same lead pool during that period. This reflects Beeline’s specific implementation, lead mix, and internal benchmarks. Results for other deployments will vary, and this figure should not be interpreted as a minimum or typical outcome.

How does conversational memory improve lead conversion?

Conversational memory means the AI agent remembers who the borrower is and what they’ve discussed across multiple interactions. A borrower who browsed 30-year rates last week and returns today doesn’t start from scratch.

Bob picks up the context, references the prior conversation, and moves the relationship forward. This continuity dramatically increases engagement and conversion because borrowers feel recognized, not processed.

Can AI agents book appointments with loan officers?

Yes. MagicBlocks integrates natively with Calendly and GoHighLevel calendaring, allowing Bob to book appointments directly within the conversation. A borrower who’s qualified and ready to speak with a loan officer doesn’t need to be redirected to a separate booking page. The appointment gets booked inside the chat, in the same session.

What CRM systems integrate with mortgage AI agents?

MagicBlocks integrates with GoHighLevel (natively), HubSpot, Twilio, Calendly, and other CRMs via Zapier webhooks. Qualified lead data including all collected borrower information flows directly into the connected CRM and triggers the appropriate follow-up workflow, without manual data entry.

What ROI can lenders expect from AI sales automation?

Results vary by funnel complexity, lead volume, and traffic source. The following is a hypothetical illustration only — not a projection of guaranteed or typical outcomes: For a lender processing 1,500 leads per month at $45 average lead cost, a hypothetical improvement in conversion from 3% to 7% would represent a significant increase in revenue potential. Actual conversion improvement, if any, will depend on lead quality, market conditions, agent configuration, and team follow-up. Consult your own data when modelling ROI expectations.

Can AI handle after-hours mortgage inquiries?

This is precisely where AI provides its most outsized impact. Beeline’s data showed that 60% of their inquiries arrived after business hours. Bob was available at 2am with the same quality of conversation that a loan officer would deliver at 10am. For lenders still relying on team-dependent coverage, after-hours inquiries represent the single largest source of silent lead leakage.

| Ready to Convert More Mortgage Leads? Designing AI sales workflows for mortgage funnels can be complex. MagicBlocks helps teams structure AI agents, build qualification flows, and optimize conversations for higher lead conversion. Build AI Sales Agents for Mortgage companies at magicblocks.ai |

Want to see this in action?

See a demoRead the playbook. Now see it run.

Watch a 4-minute demo. No sales pitch. Then decide if you want to talk.