Mortgage Lead Conversion Benchmarks (2026): Industry Averages, Funnel KPIs, and Case Study

Mortgage lead conversion benchmarks in 2026 aren't a single number. They're a sequence of rates across a funnel — contact rate, application rate, pre-approval rate, and funded-loan rate — that differ significantly by lead source, product type, and team model.

Discover 2026 mortgage lead conversion benchmarks and learn how AI sales agents are transforming performance across the industry. Optimize your funnel today.

On this page 11

- What Mortgage Lead Conversion Benchmarks Mean in 2026

- The Core Mortgage Funnel KPIs to Track

- Mortgage Lead Conversion Benchmarks by Lead Source and Channel

- Purchase vs. Refinance Benchmarks in 2026

- Benchmarks by Team Type

- What’s Changing Mortgage Lead Conversion Rates in 2026

- How AI Sales Agents Are Shifting Mortgage Conversion Benchmarks

- Beeline Case Study: What Above-Benchmark Mortgage Conversion Looks Like

- How to Build a 2026 Mortgage Lead Conversion Benchmark Report

- Frequently Asked Questions

- The Benchmark That Matters in 2026

Mortgage lead conversion benchmarks in 2026 aren’t a single number. They’re a sequence of rates across a funnel — contact rate, application rate, pre-approval rate, and funded-loan rate — that differ significantly by lead source, product type, and team model.

The teams posting above-benchmark performance aren’t just generating more leads. They’re closing the four operational gaps where most funnels leak: slow response, poor qualification, inconsistent follow-up, and dormant CRM leads that were never properly worked.

In Beeline’s deployment of an AI sales agent on their web chat channel, that approach produced six times higher lead conversion rates and eight times more mortgage applications than Beeline’s own prior internal benchmarks — without adding incremental operational cost. Results reflect Beeline’s specific implementation and will vary for other lenders.

What Mortgage Lead Conversion Benchmarks Mean in 2026

Most mortgage teams think they have a lead problem. They’re spending on paid search, aggregator feeds, and referral networks and the pipeline still looks thin. The leads are there. The conversion is what’s broken.

Mortgage lead conversion isn’t one number. It’s a sequence of rates across a funnel, each one multiplying or compressing the next. Contact rate. Application rate. Pre-approval rate. Funded-loan rate. If you’re only tracking “closed loans / total leads,” you’re flying blind.

A 5% close rate on low-quality aggregator leads looks identical to a 5% close rate on high-intent organic referrals and they’re not even close to the same problem.

In 2026, a benchmark without segmentation is close to useless. The right question isn’t “what’s a good mortgage conversion rate?” It’s: which stage, which source, which segment, which team model and compared to what?

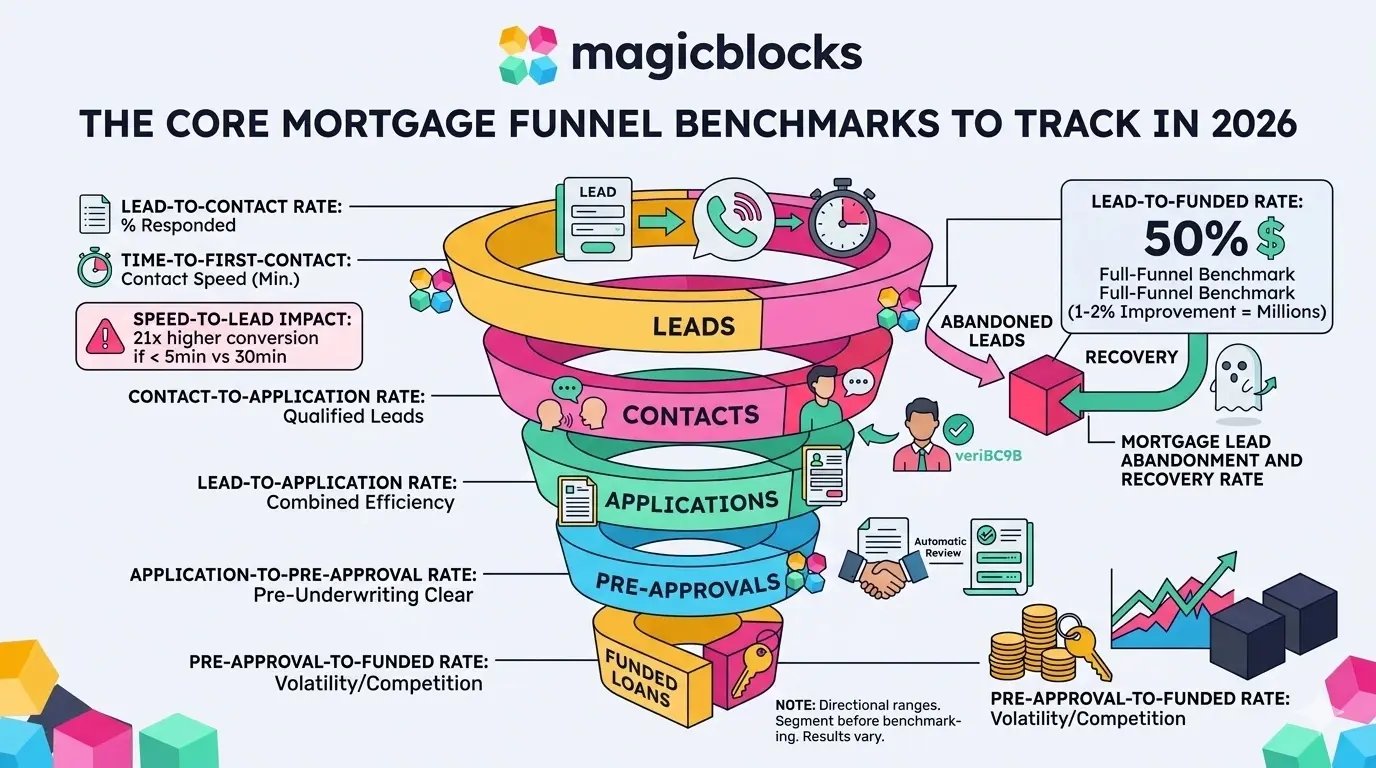

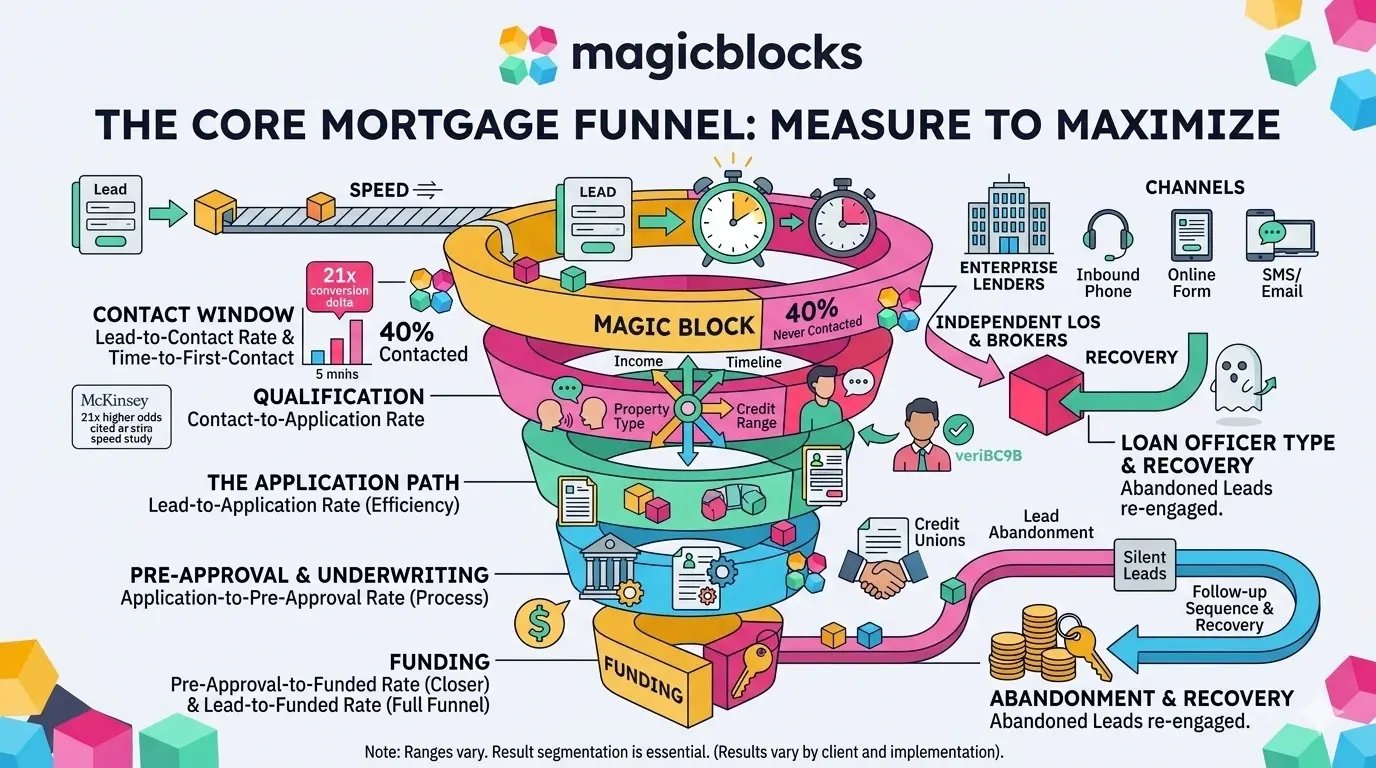

The Core Mortgage Funnel KPIs to Track

Before you can benchmark anything, you need to agree on what you’re measuring. Here’s the framework enterprise lenders, independent brokers, and credit unions should all be running:

Lead-to-contact rate

What percentage of new leads respond within the first contact window? A speed-to-contact study by Insellerate, conducted on companies attending the MBA Annual Conference, found that 40% of new mortgage leads were never contacted at all, less than 2% received a call within the first hour, and the average response time was 6 hours.

The same research found the odds of converting a lead are 21x higher if contacted within 5 minutes versus 30 minutes.

Time-to-first-contact

The clock starts the moment a lead submits. Speed-to-lead is one of the clearest predictors of whether a conversation happens at all.

Contact-to-application rate

Of the leads you actually reach, how many start an application? This is where qualification quality shows up, asking the right questions early (income, property type, credit range, timeline) converts more contacts into applications.

Application-to-pre-approval and lead-to-funded rates

The full-funnel benchmark. In high-volume environments, a 1–2% improvement in lead-to-funded rate can represent millions in additional origination.

Enterprise lenders should also track mortgage lead abandonment and recovery rate, what percentage of leads went silent, and how many re-engaged after a follow-up sequence.

Quick benchmark note: These ranges vary widely by lead source, product type, and team model. Always segment before benchmarking. Results vary by client and implementation.

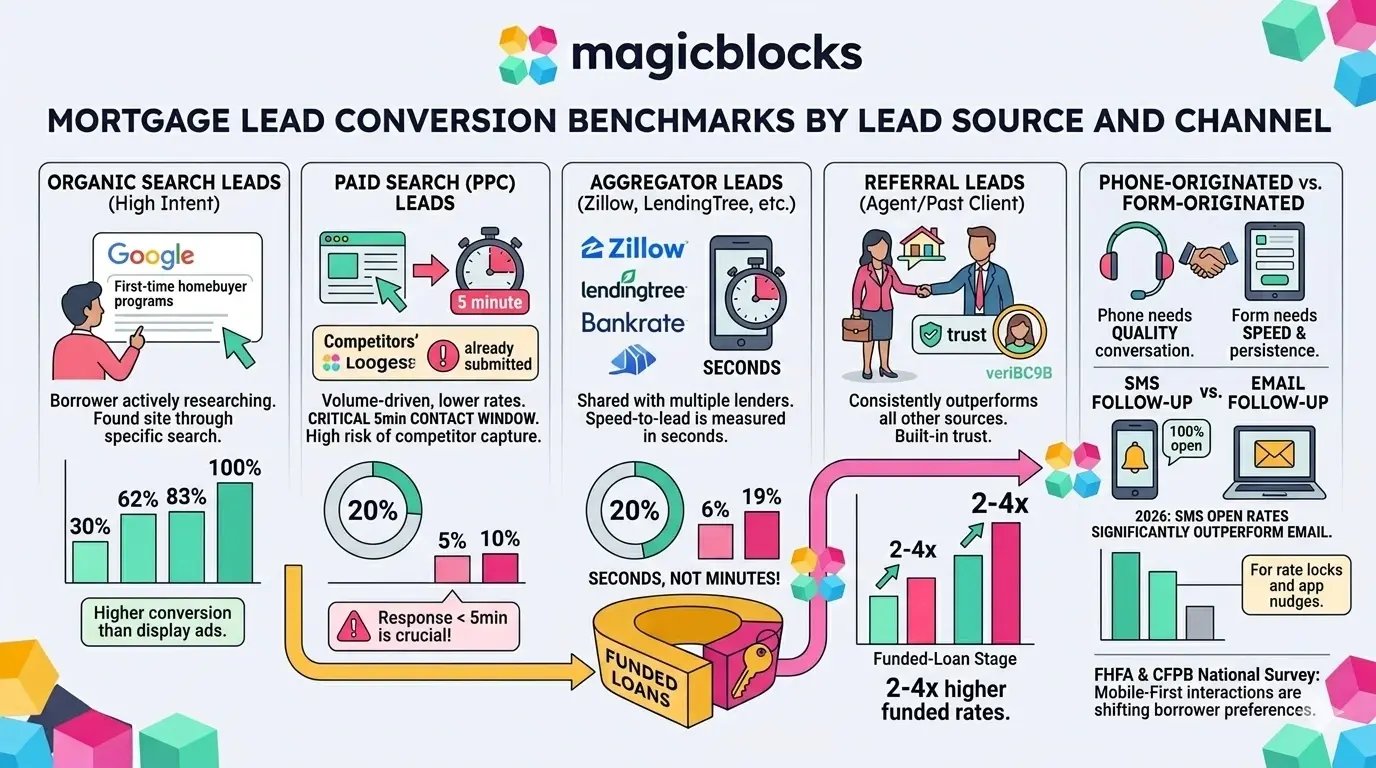

Mortgage Lead Conversion Benchmarks by Lead Source and Channel

Not all leads are created equal. The source determines the intent and intent determines what conversion rates are realistic.

| Lead Source | Contact Rate | Application Rate | Key Characteristic |

| Organic Search | Higher | Higher | Highest intent, actively researching |

| Paid Search | Moderate | Moderate | Speed-to-lead critical; high competitive volume |

| Aggregator | Low–Moderate | Lower | Shared with competitors; seconds count |

| Referral | High | Highest | Trust-based; 2–4x funded-loan rate vs. paid |

| SMS Re-engagement | Variable | Variable | Depends on lead age and sequence quality |

On channel: SMS open rates continue to significantly outperform email for mortgage follow-up sequences in 2026.

Borrowers are more likely to respond to a text than an email, particularly for time-sensitive inquiries like rate locks and application nudges.

The FHFA and CFPB National Survey of Mortgage Originations tracks how borrower channel preferences are shifting toward mobile-first interactions.

Purchase vs. Refinance Benchmarks in 2026

This is a segmentation failure that quietly poisons benchmarks for many teams. Purchase and refinance leads should never be benchmarked together.

Purchase leads carry urgency baked in a contract, a move-in date. Conversion rates from application to funded loan tend to be higher when the borrower is committed.

Refinance leads are rate-sensitive and comparison-shopping by nature. In the current rate environment, many refi inquiries are exploratory, and lead-to-application rates run lower than purchase.

Benchmarks from 2021’s refi boom are irrelevant for 2026 planning. Teams setting refi conversion targets should be using data from comparable rate environments, not historical peaks.

If your benchmark report blends purchase and refi conversion rates, it’s telling you a story that doesn’t exist. Segment first. Then benchmark.

Benchmarks by Team Type

Enterprise lenders

Enterprise mortgage lenders have more data, such as multiple channels, hundreds of loan officers, years of cohort history. The right benchmarks here are segmented by branch, channel, LO, and lead source simultaneously.

For enterprise lenders specifically, lead response infrastructure is often the biggest conversion gap. A 500-person operation with a 15-minute average response time is systematically leaking revenue that a centralized AI sales agent deployment can recover.

Independent loan officers and small brokers

Volume is lower, so each lead matters more. The benchmark failure here is usually follow-up depth: most solo operators give up after two or three attempts.

If you’re paying $50–$150 per aggregator lead and closing 1 in 30, improving follow-up from 2 touches to 8–10 touches — without adding headcount — is where the leverage lives.

Credit unions and remote LOs

Credit unions often have strong brand trust but slower operational tempo. Remote and phone-based LOs typically have higher contact attempt rates but need better digital follow-up infrastructure to compensate for the lack of face-to-face relationship-building.

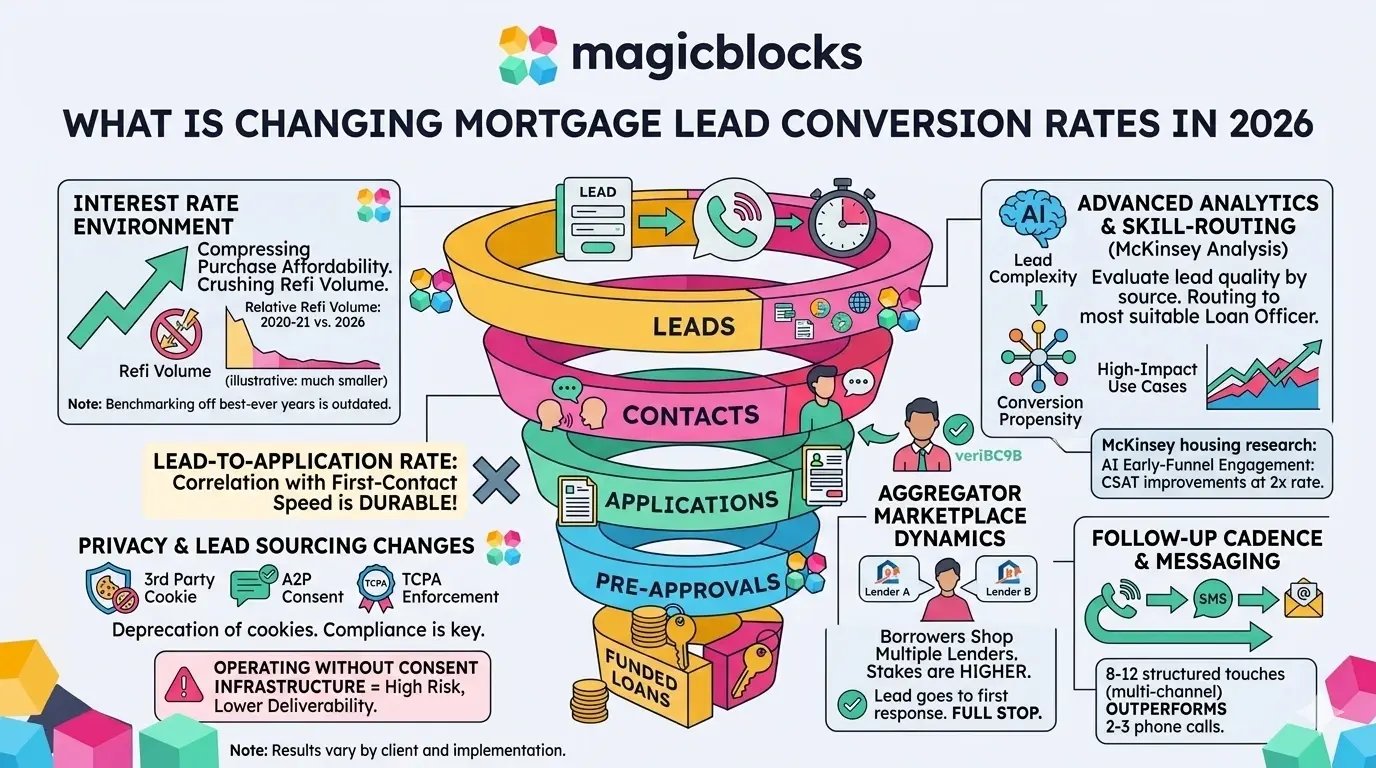

What’s Changing Mortgage Lead Conversion Rates in 2026

Several forces are compressing or shifting benchmarks simultaneously:

- Interest rate environment: Elevated rates have reduced purchase affordability and crushed refi volume relative to 2020–2021. Teams benchmarking against their best-ever year are comparing against a market that doesn’t exist anymore.

- Privacy changes: Third-party cookie deprecation, TCPA enforcement, and A2P SMS compliance requirements have made certain channels more expensive and restricted.

- Aggregator marketplace dynamics: Borrowers increasingly shop multiple lenders through comparison platforms. A lead submitted to three lenders simultaneously goes to the one who responds first.

- Follow-up cadence: Structured multi-touch sequences — typically in the 8–12 contact range across channels — are consistently associated with higher conversion than 2–3 attempt sequences.

McKinsey’s analysis of advanced analytics in mortgage originations highlights lead quality evaluation and skill-based routing as high-impact use cases.

McKinsey’s research on AI-enabled housing ecosystems also found that institutions integrating AI into early-funnel engagement see customer satisfaction improvements at twice the rate of those using conventional models.

How AI Sales Agents Are Shifting Mortgage Conversion Benchmarks

The biggest operational shift in mortgage conversion over the last 18 months is the deployment of AI sales agents as the first-response and follow-up layer between lead generation and human loan officers. Here’s what that shift actually changes:

→ Response time goes from minutes to seconds. Human-staffed operations typically respond in 8–15 minutes during business hours and much longer outside of them. An AI sales agent responds within seconds of lead submission, regardless of time of day or volume spike.

→ Qualification happens in the conversation. A well-configured AI sales agent asks about income range, property type, purchase timeline, and credit situation. It routes qualified leads to calendar booking and unqualified leads to longer nurture sequences. Loan officers receive contacts who are already pre-screened.

→ Follow-up becomes systematic. AI sales agents run 8–12 follow-up touches across web chat and SMS without dropping the ball. No lead falls through a CRM because a loan officer got busy.

→ Dead databases become active pipelines. Industry estimates suggest 70% of CRM leads were never followed up adequately. An AI-driven re-engagement sequence can recover a meaningful portion — the proportion varies significantly by lead age, original source, and outreach quality.

MagicBlocks is an AI Sales Agent built specifically for high-intent conversion funnels like mortgages. Its AI sales agents deploy the HAPPA sales framework — Hook, Align, Personalise, Pitch, Action — a five-stage methodology developed through $200M+ in lead generation experience across mortgage and other high-ticket industries.

The architecture includes a Dynamic Journey Engine that computes the next best action in real time based on the lead’s behavior, lifecycle position, and channel preference.

The engine adapts — switching from web chat to SMS, adjusting qualification depth based on intent signals, escalating to calendar booking when the lead is ready.

For enterprise mortgage operations specifically, MagicBlocks includes configurable AI guardrails (“Guardians”) that control how agents respond — helping enforce brand voice, messaging constraints, and operational rules across conversations. These rules can be tailored to support compliance-sensitive workflows, but regulatory compliance remains the responsibility of the lender and their legal counsel.

MagicBlocks holds SOC 2 and ISO 27001:2022 certifications, verifiable at trust.magicblocks.ai. The platform also maintains conversation history and lead data across sessions, allowing agents to reference prior interactions and support more contextual follow-ups.

This enables more continuous, personalized conversations with returning leads. MagicBlocks is designed as scalable infrastructure for deploying AI agents across channels, supporting high-volume lead engagement for teams operating across multiple time zones.

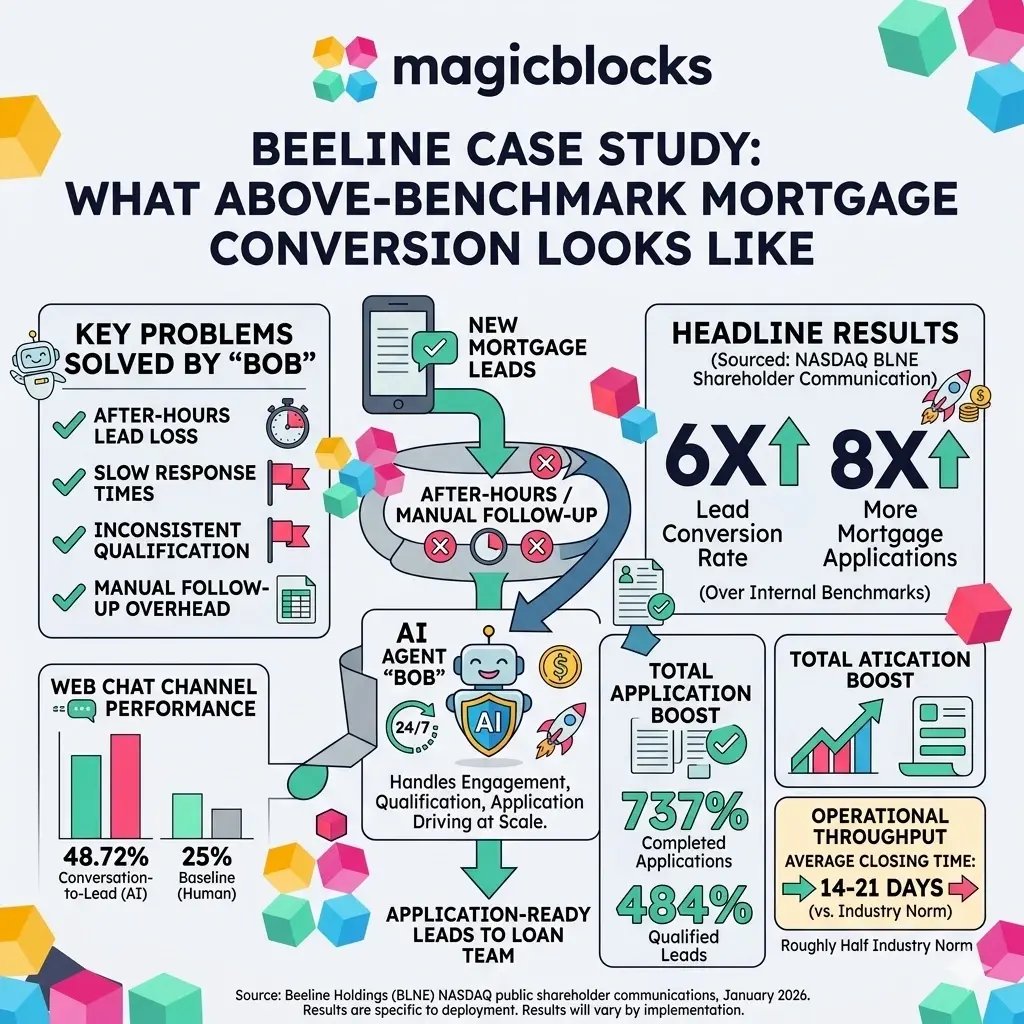

Beeline Case Study: What Above-Benchmark Mortgage Conversion Looks Like

Beeline Holdings (NASDAQ: BLNE) is a fully digital mortgage lender operating in the U.S. In 2025, Beeline deployed an AI agent called “Bob” powered by MagicBlocks to handle mortgage lead engagement, qualification, and application driving at scale.

Bob ran 24/7, responded within seconds of lead submission, guided borrowers through pre-qualification conversations, and routed application-ready leads directly to Beeline’s loan team.

According to Beeline’s CEO Nick Liuzza in a January 2026 shareholder letter, “Bob” generated six times higher lead conversion rates and eight times more mortgage applications than Beeline’s internal benchmarks without adding incremental operational cost.

The Beeline case study at MagicBlocks details the operational mechanics: a 737% increase in completed applications and 484% growth in qualified leads, with a 48.72% conversation-to-lead rate on the web chat channel — compared to Beeline’s prior 25% human-agent baseline on the same channel. Results reflect Beeline’s specific deployment, team configuration, and market conditions and will vary by implementation.

What mortgage teams can learn from the Beeline playbook

- 24/7 first response removes the biggest single drop-off point in most mortgage funnels.

- Conversational pre-qualification — asking about property type, loan size, timeline, and credit range in natural conversation rather than a static form — dramatically improves application quality and loan officer efficiency.

- After-hours lead capture via web chat recovers leads that would otherwise sit in a CRM until the next business morning, by which point they’ve already applied elsewhere.

- CRM and calendar integration means qualified leads arrive in the loan officer’s workflow already pre-screened and ready to book.

Beeline should be read as an above-benchmark case study, not an average. The mechanics behind it are replicable.

For enterprise lenders and growth-stage mortgage operations looking at how AI sales agents increase mortgage lead conversion,

MagicBlocks is the conversion layer between traffic and loan staff: instant first response, guided qualification, structured follow-up, and measurable benchmark improvement against existing funnel data.

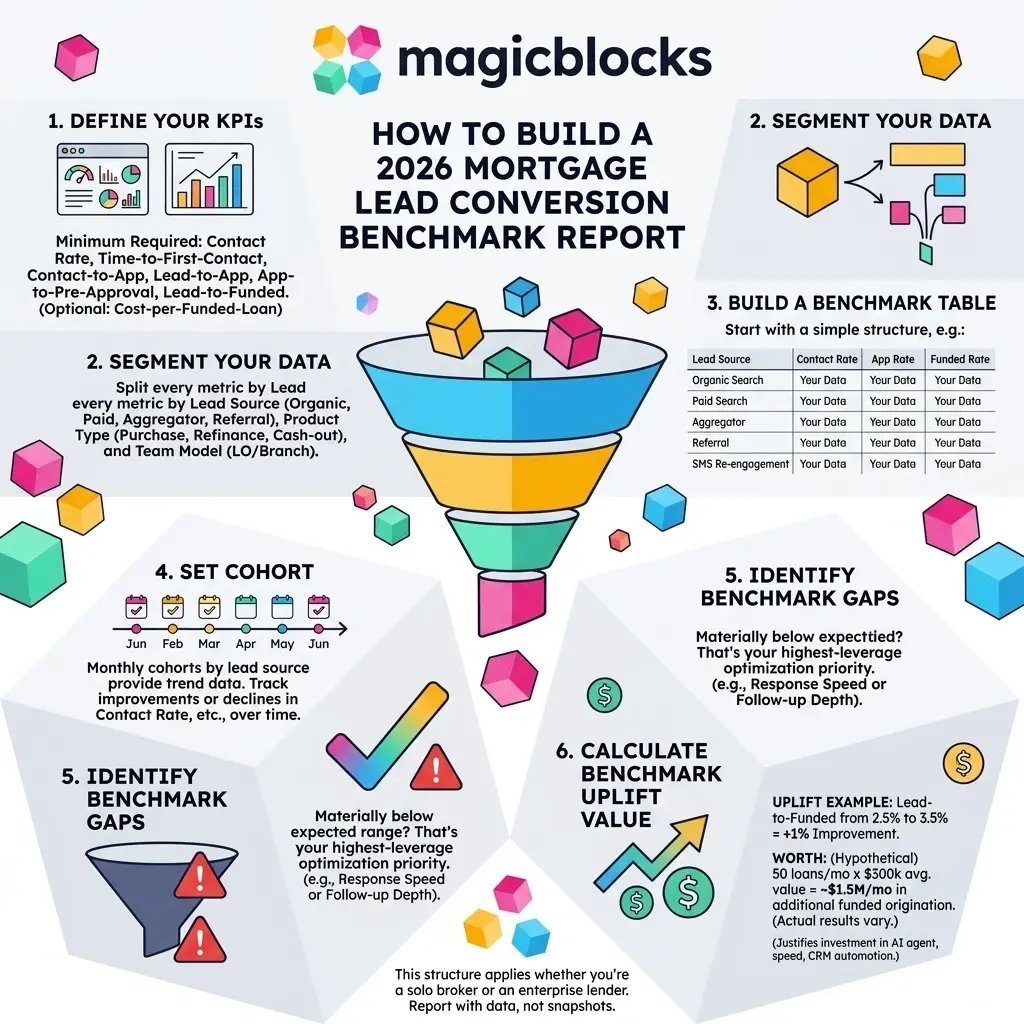

How to Build a 2026 Mortgage Lead Conversion Benchmark Report

This structure applies whether you’re a solo broker or an enterprise lender with 200+ LOs:

- Define your KPIs. At minimum: contact rate, time-to-first-contact, contact-to-application rate, lead-to-application rate, application-to-pre-approval rate, and lead-to-funded rate.

- Segment before you benchmark. Split every metric by lead source (organic, paid, aggregator, referral), product type (purchase, refinance, cash-out), and team model. Blended numbers mislead.

- Set cohort timelines. Monthly cohorts by lead source give you trend data, not snapshots.

- Identify benchmark gaps. Where are you materially below the segment’s expected range? For most teams, it’s either response speed at the top of the funnel or follow-up depth in the middle.

- Calculate benchmark uplift value. A team funding 50 loans per month at $300,000 average loan value would see approximately $1.5M in additional monthly origination from a single percentage point of conversion improvement. Actual results depend on your specific funnel, lead volume, loan mix, and operational execution.

Frequently Asked Questions

What are typical mortgage lead conversion rates in 2026?

There’s no single “typical” rate — conversion depends heavily on lead source, product type, response infrastructure, and team model. Contact rates for aggregator leads can fall below 30% without fast response infrastructure. Referral leads can convert at 3–5x those rates. The right benchmark is segmented, not blended.

What is a good mortgage lead-to-application rate in 2026?

In Beeline’s specific AI-assisted deployment on their web chat channel, a 48.72% conversation-to-lead rate was achieved compared to Beeline’s prior 25% human-agent baseline on the same channel. This is an above-benchmark result from a specific implementation — don’t use it as a general benchmark. For most operations, meaningful improvement begins with faster first response and more persistent follow-up sequences.

How quickly should mortgage teams contact new leads in 2026?

Within five minutes, at minimum and faster is better. After-hours lead capture via AI sales agents is now a meaningful competitive variable: a lead submitted at 9pm that gets a response in 60 seconds converts at materially higher rates than one that waits until 8am the next morning.

How do AI sales agents affect mortgage lead conversion benchmarks?

AI sales agents shift the benchmarks by closing the biggest gaps in the funnel: slow response, inconsistent follow-up, and underworked CRM leads. For most operations, the measurable lift shows up first in contact rate (faster response = more conversations) and then in application rate (better qualification = more completed applications).

How should enterprise lenders benchmark conversion by channel and cohort?

Enterprise lenders should run cohort analyses segmented by lead source, product type, LO/branch, and entry month. Cross-channel benchmarks — web chat vs. SMS vs. inbound phone — reveal where response infrastructure is creating conversion variance. AI sales agents operating across web chat and SMS create a consistent first-response layer that reduces variance across LOs and branches.

How should small mortgage brokers set 2026 conversion goals?

Start with your cost-per-funded-loan target and work backward. If you’re funding 5 loans per month from 300 leads, your current lead-to-close rate is 1.67%. A realistic near-term goal — achievable with better follow-up depth and faster response — is 2.5–3%. Translate that into funded loan revenue per month to understand the value of the improvement, then build your improvement plan around the specific funnel stage with the biggest gap.

The Benchmark That Matters in 2026

The 2026 benchmark isn’t a single rate. It’s a framework for finding where your funnel is leaking — and fixing it before you spend another dollar on lead generation.

The conversion levers are clear: faster response, smarter qualification, persistent follow-up, and dead database reactivation. Beeline’s deployment is the clearest proof point available that AI sales agents can drive above-benchmark performance on all four simultaneously.

MagicBlocks is built for exactly this. Create your AI Sales Agent at magicblocks.ai and start converting the leads you’ve already paid for.

Statistics sourced from Beeline’s public NASDAQ shareholder communications and the MagicBlocks case study page reflect specific client deployments. Results vary by implementation, team configuration, lead source, and market conditions. This article is intended for mortgage and lending professionals and does not constitute financial, legal, or regulatory advice. Consult qualified legal counsel regarding compliance obligations applicable to your operations.

Want to see this in action?

See a demoRead the playbook. Now see it run.

Watch a 4-minute demo. No sales pitch. Then decide if you want to talk.