Top AI Tools for Mortgage Lead Generation Agencies (2026 Edition)

If you run a mortgage lead generation agency in 2026, you don't need "more tools."

Discover the top AI tools revolutionizing mortgage lead generation in 2026, focusing on intelligent automation, relationship continuity, and instant qualification to boost conversions.

On this page 8

- Why Mortgage Lead Generation Is Different

- What Most “AI Mortgage Tools” Get Wrong

- The Shift: From Tools to Autonomous Relationship Sales

- MagicBlocks.ai – AI That Actually Sells Mortgages

- Other AI Tools Worth Considering (With Context)

- What Winning Mortgage Agencies Are Doing in 2025

- Final Take

- Frequently Asked Questions

If you run a mortgage lead generation agency in 2026, you don’t need “more tools.”

You need four AI capabilities working together:

| Category | What It Solves | Example |

| AI Sales Agents | Convert inbound leads instantly | MagicBlocks.ai |

| CRM + Automation | Pipeline tracking & follow-up | HubSpot, GoHighLevel |

| AI Personalization | Email + SMS customization at scale | Instantly, Smartlead |

| Predictive Lead Scoring | Prioritize high-intent borrowers | Clearbit, Apollo.io |

But here’s the real problem:

Most agencies stack tools.

The agencies seeing strong results tend to integrate tools that work together as a cohesive system. Some mortgage agencies are consolidating multiple point solutions into a single AI-led workflow — though outcomes depend heavily on implementation, team adoption, and lead quality.

According to McKinsey’s 2023 research on mortgage borrower preferences highlights that interaction frequency during the exploration phases is associated with higher satisfaction. This points to the value of sustained nurture — though the research focuses on borrower satisfaction rather than directly measuring commission outcomes for agencies.

The same research reveals that just over half of borrowers consider only a single institution in their search for a mortgage, making speed-to-lead and instant qualification critical competitive advantages.

Meanwhile, S&P Global notes that agentic AI adoption in mortgage origination represents a significant infrastructure shift, moving beyond simple automation toward autonomous relationship management systems.

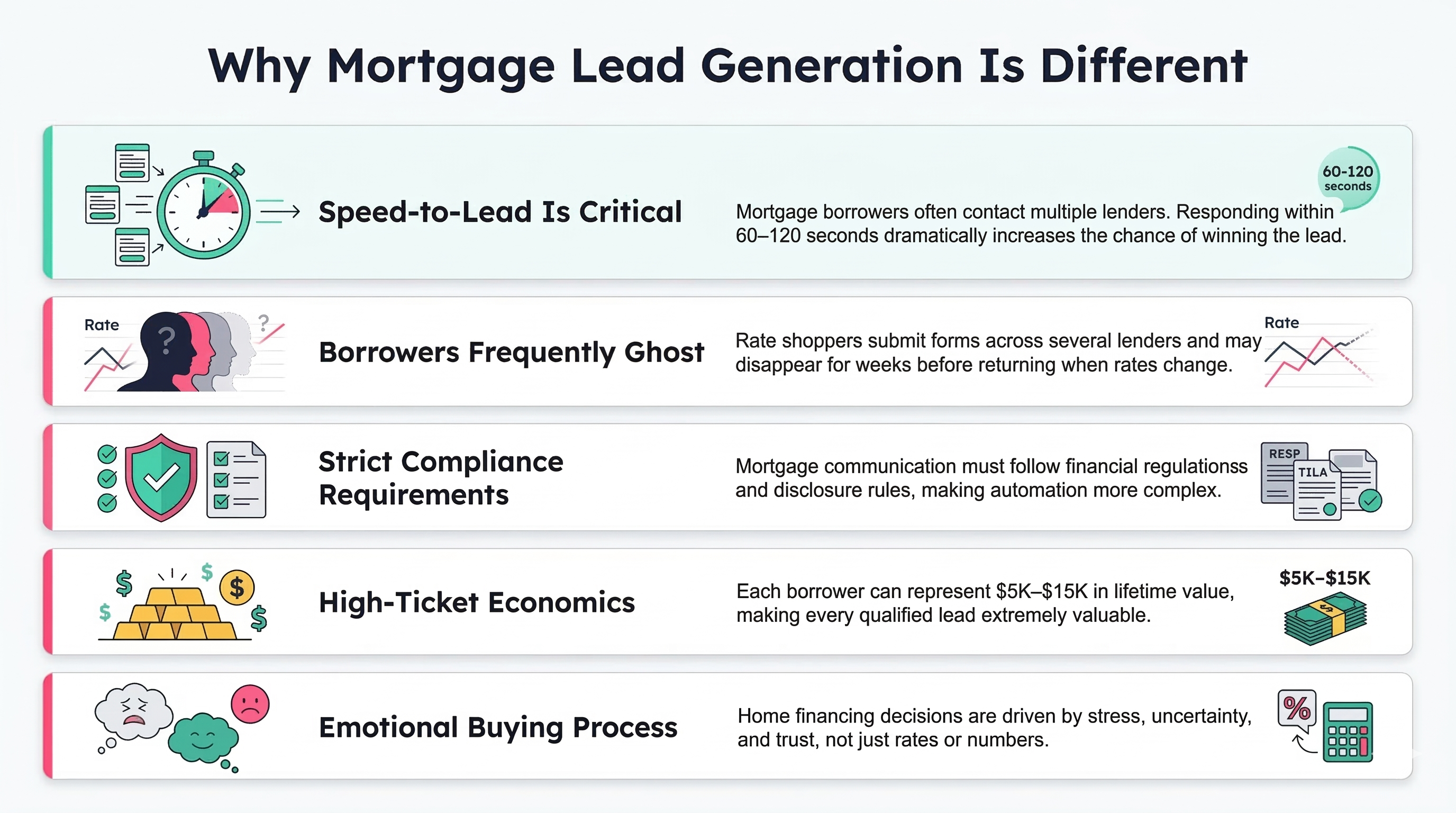

Why Mortgage Lead Generation Is Different

Mortgage lead gen isn’t SaaS.

It’s not ecommerce.

It’s emotional. High-ticket. Regulated. And extremely time-sensitive.

Here’s what makes mortgage leads uniquely hard:

Speed-to-Lead Is Everything

If you don’t respond in 60–120 seconds, the borrower talks to someone else.

McKinsey data shows that only about half of borrowers even consider multiple lenders. When someone submits a mortgage inquiry form, they’re often already talking to two other companies. The winner isn’t the one with the best rates — it’s the one who responds first with actual value.

-

Borrowers Ghost Constantly

Rate shoppers submit 3–5 forms across different lenders.

They disappear. Then reappear weeks later when rates shift or their home search progresses.

Most CRM systems treat this as “lead death.” Smart AI treats it as part of the natural mortgage buying cycle and maintains nurture without burning out your team.

-

Compliance Matters

Mortgage communication involves financial data, disclosures, and strict regulations.

You can’t just “move fast and break things” when you’re dealing with someone’s largest financial decision. Your AI needs to handle objections intelligently while staying compliant with RESPA, TILA, and state-specific lending regulations.

-

High-Ticket Economics

Each borrower is worth $5K–$15K LTV depending on deal size and refinance cycles.

When the lifetime value is this high, manual follow-up seems justified. But here’s the problem: your loan officers are spending 70% of their time chasing unqualified leads instead of closing ready buyers.

-

Emotional Buying Process

Buying or refinancing a home isn’t logical.

It’s fear-driven:

- “Am I getting the best rate?”

- “Is now the right time?”

- “What if I mess this up?”

You don’t need another email tool.

You need AI that understands how people make financial decisions under stress.

What Most “AI Mortgage Tools” Get Wrong

There’s a huge difference between:

AI that answers questions

vs.

AI that sells mortgages

Here’s where most platforms fail:

Stateless Conversations

They don’t remember context from previous interactions.

A borrower asks about refinancing on Monday, clicks away, returns Thursday asking about purchase loans — and the AI treats them like a brand new lead. No continuity. No relationship building. No trust.

No Memory Across Channels

SMS and chat operate separately. Email is its own silo.

Your borrower starts a conversation via website chat, gets a text follow-up, then receives an email — and each channel treats them like they’ve never interacted with your company before.

One-Channel Communication

Email-only or SMS-only systems miss borrower intent signals.

Some borrowers want to text. Others prefer email. Many start on your website and need omnichannel follow-up that feels like the same intelligent conversation, not three different bots.

No Objection Handling

Rate comparison? Credit score hesitation? Timing fear?

Generic bots freeze.

Real mortgage sales require addressing specific objections:

- “I’m shopping around for rates” → Needs comparison framework

- “My credit isn’t great” → Needs reassurance about approval options

- “Is now the right time?” → Needs market timing education

- “The paperwork seems overwhelming” → Needs process clarity

Cookie-cutter chatbots can’t navigate these conversations. They collect information. They don’t sell.

No Longitudinal Nurture

Most borrowers convert in 30–90 days.

Most tools stop at Day 3.

McKinsey’s research confirms that customer satisfaction increases significantly with frequency of interactions, especially during the exploration phase. But traditional tools send three automated emails and then go silent, leaving thousands of dollars in potential commission on the table.

That’s why stacking CRM + SMS + Email + AI copy tools still feels fragmented.

You’re managing four systems when what you actually need is one intelligence layer that remembers, learns, and sells.

The Shift: From Tools to Autonomous Relationship Sales

Mortgage agencies don’t need more automation.

They need: Autonomous Relationship Sales Infrastructure.

Instead of:

- CRM doing tracking

- Email tool doing blasts

- VA doing follow-ups

- Loan officer doing manual texting

One intelligent system should:

✅ Respond instantly (under 5 seconds)

✅ Qualify intelligently (credit, geography, intent)

✅ Handle objections (rate shopping, timing, paperwork fears)

✅ Nurture long-term (30-90 day cycles automatically)

✅ Book consults automatically (qualified leads only)

This is the architecture winning mortgage agencies are building in 2025.

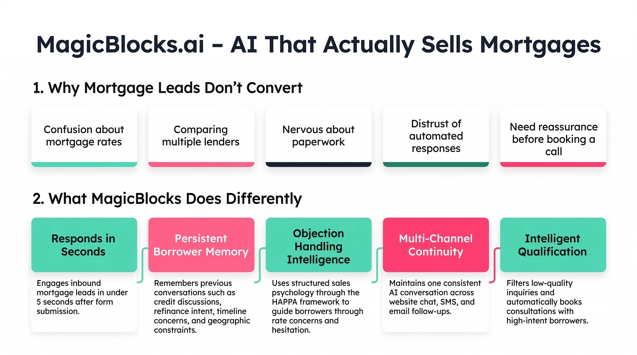

MagicBlocks.ai – AI That Actually Sells Mortgages

Why Mortgage Leads Don’t Convert

Mortgage leads usually stall because:

- They’re confused about rates

- They’re comparing multiple lenders

- They’re nervous about paperwork

- They don’t trust automated responses

- They need reassurance before booking a call

Traditional tools send reminders.

MagicBlocks sells clarity.

What MagicBlocks Does Differently

-

Responds in Seconds

Captures inbound Facebook, Google, or landing page leads instantly.

While manual lead routing can take 10 minutes or more, MagicBlocks is designed to engage borrowers within seconds of form submission. Faster response times are widely associated with improved engagement in high-intent verticals, though actual conversion rate impact varies by lead source, market, and follow-up quality.

-

Remembers Past Interactions

Maintains memory across conversations:

- Credit score discussion from last week

- Refinance vs. purchase intent

- Timeline concerns

- Rate sensitivity

- Geographic constraints

This isn’t just “conversation history.” It’s a CDP-native memory engine that treats each borrower as a longitudinal relationship, not a series of disconnected interactions.

-

Handles Objections

Not just: “Would you like to book a call?”

But: “I understand rate shopping is important — here’s how we help you compare intelligently while ensuring you get pre-approved so you can make competitive offers.”

MagicBlocks agents are built on the HAPPA Framework (Hook → Align → Personalize → Pitch → Action), a sales psychology methodology developed through the MagicBlocks team’s combined prior experience across lead generation work in mortgage and other high-ticket industries.

They don’t improvise. They follow proven objection-handling playbooks specific to mortgage psychology.

-

Multi-Channel Continuity

SMS + Web Chat + Email follow-up flows operate in sync.

Borrower starts on your website at 11 PM asking about refinancing. MagicBlocks captures intent, books them for a consultation, then follows up via text the next morning with rate information and a calendar link — all as the same consistent AI agent, not three different systems.

-

Books Qualified Calls Automatically

Filters out:

- Low credit (below your minimums)

- Wrong geography (outside your lending area)

- Non-serious inquiries (just browsing)

And books:

- Ready-to-close borrowers

- Warm consults with documented income

- High-intent refinancers with equity positions

This qualification approach is designed to help loan officers spend more time on higher-intent conversations and less time on unqualified follow-up. The proportion of time redirected depends on your current lead mix, qualification criteria, and agent configuration.

Built on Sales DNA (Not Just Prompts)

Unlike generic AI wrappers, MagicBlocks is structured around:

✅ Sales playbooks (mortgage-specific scripts)

✅ Financial psychology (understanding borrower fears)

✅ HAPPA-style persuasion sequencing (proven over $200M in leads)

✅ Mortgage-specific objection libraries (rate anxiety, credit concerns, timing hesitation)

For mortgage agencies, that means:

Turning rate shoppers into booked consults automatically.

And reducing the need for:

- Call center staff ($40K–$60K per rep annually)

- Manual follow-up VAs ($3K–$5K monthly)

- Multi-tool stitching (CRM + SMS + Email + Chatbot subscriptions)

One system. One memory. One continuous sales conversation.

Other AI Tools Worth Considering (With Context)

CRM & Pipeline: HubSpot vs. GoHighLevel

HubSpot → Enterprise-level reporting & integrations

GoHighLevel → Agency-focused all-in-one marketing CRM

Both are strong pipeline management platforms. HubSpot excels at complex deal tracking and attribution modeling. GoHighLevel dominates the agency white-label market with built-in client management.

But neither replaces AI-led selling.

They organize leads. They track stages. They remind your team to follow up.

They don’t convert leads autonomously.

You still need someone (human or AI) doing the actual selling. That’s where most agencies hit the bottleneck — they’ve got leads organized beautifully in their CRM, but nobody’s actually moving them toward a booked consultation.

AI Outreach Tools: Instantly & Smartlead

These tools help with:

- Cold email outreach

- Email warm-up (domain reputation management)

- Campaign scaling across multiple inboxes

Instantly and Smartlead are excellent for B2B cold outreach where you’re initiating contact.

But mortgage leads aren’t cold outbound.

They’re inbound emotional decisions.

Someone filling out a “get my rate” form is already warm. They’re already interested. They don’t need six drip emails — they need intelligent qualification and objection handling within the first 120 seconds.

Personalization ≠ persuasion.

Merge tags that insert don’t build trust. Remembering that Sarah asked about FHA options last Tuesday and following up with specific FHA rate updates — that builds trust.

Predictive Lead Scoring: Clearbit & Apollo

Great for B2B data enrichment.

Clearbit excels at firmographic data. Apollo provides contact information and intent signals for companies.

But mortgage is B2C — and intent changes daily.

Someone not ready to refinance today might be ready next week when rates drop 25 basis points. Predictive scoring based on job title and company size doesn’t capture mortgage-specific buying signals like:

- Recent home search activity

- Credit score improvement

- Rate sensitivity timing

- Equity position changes

Lead scoring helps prioritize.

It doesn’t build trust or move borrowers toward decisions.

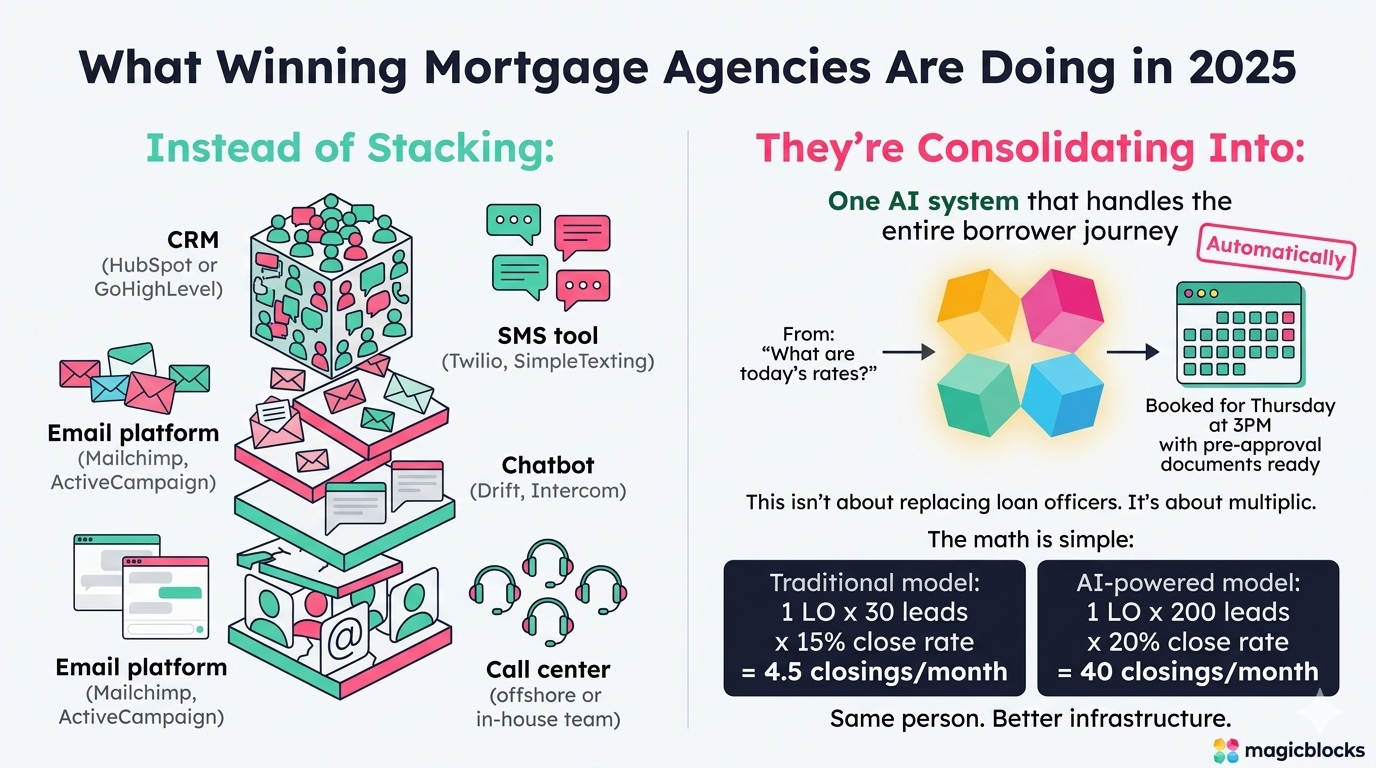

What Winning Mortgage Agencies Are Doing in 2025

Instead of stacking:

- CRM (HubSpot or GoHighLevel)

- SMS tool (Twilio, SimpleTexting)

- Email platform (Mailchimp, ActiveCampaign)

- Chatbot (Drift, Intercom)

- Call center (offshore or in-house team)

They’re consolidating into:

One AI system that handles the entire borrower journey.

From:

“What are today’s rates?”

To:

“Booked for Thursday at 3PM with pre-approval documents ready.”

Automatically.

This isn’t about replacing loan officers. It’s about multiplication.

AI-assisted qualification can allow loan officers to manage a larger active lead pool than manual-only workflows — some agencies report their LOs handling significantly more concurrent relationships. Actual capacity increase depends on lead quality, system configuration, and your team’s process. Individual results will vary.

For illustrative purposes only — actual results vary by loan officer, market, lead quality, and implementation:

- Traditional model: 1 LO × 30 leads × 15% close rate = 4.5 closings/month.

- AI-assisted model: 1 LO × 200 leads × 20% close rate = 40 closings/month.

These figures are hypothetical examples to illustrate the potential impact of lead volume and conversion improvements — not a representation of typical or guaranteed outcomes. Actual lead capacity, close rates, and revenue will differ.

Final Take

Most AI tools answer questions.

Very few actually sell mortgages.

If you’re running a mortgage lead generation agency in 2025, the competitive advantage isn’t more software.

It’s intelligent automation that understands financial psychology, emotional buying behavior, and long sales cycles.

The agencies that win won’t have more tools.

The agencies that win will have more integrated systems —

consolidating fragmented tech stacks into AI-assisted workflows that maintain borrower context, support objection handling, and facilitate consultation booking. No system handles every scenario autonomously; human oversight and escalation remain essential, particularly for complex borrower situations.

Because at the end of the day, mortgage leads don’t care about your CRM architecture or your email platform.

They care about feeling understood, getting clear answers fast, and moving toward homeownership without friction.

Give them that experience, and you win.

Make them wait, repeat themselves, or navigate three disconnected systems — and they’re already talking to your competitor.

The choice is yours.

Create free AI agent with MagicBlocks for your mortgage lead generation agency and your clients.

Frequently Asked Questions

What is the best AI tool for mortgage lead conversion?

The best AI tool combines instant response (under 5 seconds), intelligent objection handling (addressing rate anxiety, credit concerns, timing hesitation), and omnichannel follow-up (SMS, chat, email in sync).

Platforms like MagicBlocks.ai stand out because they focus on sales intelligence and relationship continuity, not just automation. Unlike generic chatbots that answer questions, effective mortgage AI actively qualifies borrowers, handles financial psychology objections, and books consultations automatically.

Can AI qualify mortgage leads automatically?

Yes. Modern AI sales systems can automatically qualify mortgage leads by asking targeted questions about credit score ranges, confirming location eligibility, understanding purchase versus refinance intent, verifying income documentation readiness, and assessing timeline urgency.

The system then routes qualified leads directly to calendar booking while nurturing not-yet-ready leads over 30-90 day cycles. This type of automated qualification workflow is designed to reduce the proportion of loan officer time spent on unqualified inquiries. The degree of time savings varies by implementation, lead source, and qualification criteria configured. Some clients have reported significant reductions in manual follow-up time, though results are not guaranteed and will differ by organization.

How does AI reduce speed-to-lead response time?

AI responds instantly — typically within seconds of form submission — eliminating the delay caused by human follow-up, manual CRM checks, or lead routing workflows. When a borrower submits a rate inquiry at 11 PM, AI engages immediately instead of waiting until business hours.

Can AI systems be deployed in a way that supports compliance with mortgage data regulations?

Yes, but AI itself is not inherently compliant or non-compliant. Compliance depends on system architecture, data handling practices, built-in guardrails, human oversight protocols, and the regulatory alignment of the deploying organization. AI must be deployed within a compliant infrastructure — it doesn’t automatically make your operations compliant just by being “AI.”

What data protection measures should mortgage AI systems include?

Effective AI systems for mortgage lead generation should follow data minimization and privacy-by-design principles:

PII Collection Control: Avoid collecting sensitive personally identifiable information unless absolutely necessary for qualification. Don’t ask for full SSNs when last four digits suffice.

Data Masking and Redaction: Automatically mask or redact sensitive data in conversation logs and CRM records. Never expose raw SSNs, full account numbers, or complete financial identifiers in AI responses or handoff documentation.

Encryption Standards: Enforce encryption in transit (TLS 1.2+) and at rest for all borrower data moving between your website, AI system, CRM, and communication channels.

Secure API Integration: All CRM connections (HubSpot, GoHighLevel, Salesforce) should use encrypted APIs with proper authentication and access controls.

The key principle: collect the minimum data required, protect what you collect, and never expose sensitive identifiers unnecessarily.

How does AI handle mortgage disclosure requirements?

AI systems must follow financial communication standards including RESPA (Real Estate Settlement Procedures Act) and TILA (Truth in Lending Act) disclosure requirements. This means:

- Maintaining conversation logs for regulatory audit trails

- Avoiding specific rate promises without proper disclaimers

- Including required disclosures when discussing loan products or payment examples

- Flagging conversations that require human loan officer review before making binding commitments

Properly configured AI can support compliance efforts through standardized messaging, audit logging, and guardrail enforcement — but it must operate within a regulated compliance framework and human oversight model. AI does not replace compliance officers, remove regulatory risk, or guarantee compliance on its own.

What certifications should agencies verify before deploying mortgage AI?

For U.S. mortgage lead generation, agencies should verify compliance with:

GLBA (Gramm-Leach-Bliley Act): The primary federal law governing financial data privacy and security in mortgage lending. Your AI vendor should demonstrate GLBA-compliant data handling practices.

SOC 2 Type II: Validates that the vendor’s systems have appropriate security controls for customer data.

State-Specific Requirements: Some states have additional data privacy laws (California CCPA, Virginia VCDPA) that may apply to mortgage lead handling.

The vendor should be able to provide documentation of their security architecture, data handling policies, and compliance frameworks. If they can’t clearly explain how they handle GLBA requirements, that’s a red flag.

What AI can replace mortgage call center staff?

Autonomous AI sales agents can replace or significantly reduce call center dependency by responding to inbound leads instantly (24/7/365), following up automatically across multiple channels (SMS, email, chat), handling common FAQs and objections (rates, credit requirements, timelines, paperwork), pre-qualifying borrowers before human handoff, and booking appointments directly into loan officer calendars.

Depending on current staffing models and lead volume, some agencies using AI-led qualification have reported reductions in per-lead follow-up costs compared to traditional call center operations. Actual cost impact varies significantly by team size, lead mix, and implementation. Results are not guaranteed. However, AI works best augmenting human loan officers for complex scenarios, not completely replacing the human element in high-trust financial decisions.

How long does it take to implement AI for mortgage lead generation?

Implementation timeframe varies by system complexity. Simple chatbot installations take 1-2 days but offer limited functionality.

Comprehensive AI sales agent platforms like MagicBlocks typically require 5-7 days for full deployment including CRM integration (HubSpot, GoHighLevel, Salesforce), SMS/email channel setup, knowledge base configuration with mortgage-specific objection handling, calendar integration for automatic booking, and custom journey design matching your sales process.

The key difference: chatbots go live fast but convert poorly; sales-focused AI takes slightly longer to configure but generates qualified appointments immediately.

What’s the ROI of AI for mortgage lead generation agencies?

The following figures represent estimated ranges based on general industry observations and illustrative scenarios — not guaranteed outcomes. Actual results will vary by agency size, lead volume, market, and implementation quality. Speed-to-lead improvement: AI response times are typically measured in seconds vs. minutes for manual follow-up. Cost per acquisition: some agencies report reductions in manual follow-up costs, though the range varies widely. Lead-to-appointment rates: improvement depends on lead quality, qualification logic, and LO follow-up. Lead management capacity: LO capacity increases vary by workflow design. Timeline to ROI: depends on pricing tier, lead volume, and close rates. Consult with our team for an estimate based on your specific situation.

Want to see this in action?

See a demoRead the playbook. Now see it run.

Watch a 4-minute demo. No sales pitch. Then decide if you want to talk.