Stop AI Agent Hallucinations in Mortgage: 7 Essential Safeguards

AI hallucinations in mortgage workflows aren't a model quality problem, they're an architecture problem.

Discover essential guardrails to prevent AI hallucinations in mortgage workflows, ensuring compliance and protecting borrower relationships in regulated environments.

On this page 13

- You Don’t Have an AI Problem. You Have a Control Problem.

- What ‘AI Hallucinations’ Actually Mean in Mortgage Workflows

- Why Mortgage Workflows Are a Zero-Tolerance Environment for AI Errors

- What Are AI Guardrails? An Operational Definition for Enterprise Teams

- The 7 Core Guardrails That Prevent Hallucinations in Mortgage AI

- How Guardrails Work Together: End-to-End Mortgage Flow

- Why Most ‘AI Chatbots’ Fail in Mortgage Use Cases

- Guardrails vs. Prompts: What Actually Prevents Hallucinations

- Business Impact: What Happens When You Get Guardrails Right

- How to Evaluate AI Guardrails in Mortgage Platforms: A Checklist

- The Future: From Chatbots to Controlled AI Sales Systems

- FAQ

AI hallucinations in mortgage workflows aren’t a model quality problem, they’re an architecture problem. When an AI system has no constraints on what it can say, no grounding in verified data, and no rules about when to stop talking, it will eventually say something that creates compliance exposure.

The solution isn’t a smarter model. It’s guardrails: a control system that defines what the AI is allowed to say, what data it can access, and what actions it’s permitted to take. Without that architecture, no AI deployment belongs in a regulated sales environment.

You Don’t Have an AI Problem. You Have a Control Problem.

Here’s the scenario. Your ops team finally gets sign-off on an AI sales agent for the mortgage funnel. The demo looked good. The vendor said it was ‘trained on finance.’ You go live.

Three weeks later, a borrower calls your LO furious. The AI told them they ‘likely qualify for a 6.1% fixed rate’ based on nothing — no credit pull, no income verification, no LTV check. The borrower locked in that expectation. You didn’t. Now you’ve got a compliance conversation you didn’t want and a borrower relationship you can’t easily repair.

That’s a hallucination. And it’s not a bug in the AI. It’s a failure in the architecture around it.

Most mortgage operations leaders hear ‘AI hallucination’ and assume it’s a model quality problem — something the vendor will fix in the next update. It isn’t. Hallucinations are what happen when an AI system has no constraints on what it can say, no grounding in verified data, and no rules about when to stop talking.

The fix isn’t a smarter model. It’s guardrails.

| In mortgage, ‘almost correct’ is legally wrong. Guardrails are the control system that makes AI usable in regulated workflows. |

This article breaks down what AI guardrails actually are, why the mortgage environment demands a zero-tolerance approach to AI errors, and how enterprise-grade AI Sales Agents — the category of AI purpose-built for lead conversion in regulated industries — implement guardrails at every layer of the stack.

What ‘AI Hallucinations’ Actually Mean in Mortgage Workflows

Let’s be precise. In the context of large language models, hallucination means the model generates output that sounds authoritative but has no factual basis. The model isn’t lying — it doesn’t have the capacity to lie. It’s predicting statistically probable word sequences. When it lacks accurate data, it fills the gap with plausible-sounding text.

Research confirms that standard LLMs frequently hallucinate when handling financial tasks. Even with access to actual financial documents, AI can distort the facts — a 6-to-1 stock split becomes a 10-to-1 split because the prediction algorithm drifts. In mortgage workflows, that drift is catastrophic.

Not Just Wrong Answers, Risky Answers

There’s a meaningful difference between an AI giving a wrong answer and an AI giving a wrong answer confidently in a regulated sales context. In mortgage, the following hallucination types create the highest exposure:

- Fabricated rates: AI quotes a specific rate or APR without any connection to current market data, the borrower’s credit profile, or product guidelines

- Incorrect eligibility logic: AI tells a borrower they qualify for a program when they don’t — or that they don’t when they do

- Outdated lending policies: AI references product criteria, loan limits, or DTI thresholds that changed months ago

- Misleading compliance statements: AI implies regulatory approval or guarantee where none exists

- Invented regulatory references: AI cites a compliance rule or exemption that doesn’t exist, phrased with complete confidence

Why AI Sounds Confident Even When It’s Wrong

This is the part that catches most mortgage ops teams off guard. LLMs are trained to produce coherent, confident responses. Confidence is baked into the output mechanism — the model doesn’t experience uncertainty the way a human does. It generates what statistically follows.

Industry hallucination rates range from 0.7% for the best-performing models to nearly 30% for smaller open-source systems. Even at the 0.7% end, that’s 7 hallucinations per 1,000 prompts. In a high-volume mortgage funnel running thousands of conversations per week, that’s not a rounding error.

The financial exposure is real. Industry data puts hallucination-related financial losses across enterprise AI deployments at over $250M annually and that figure doesn’t account for the regulatory tail.

Real Mortgage Example: Before and After Guardrails

| Scenario | Without Guardrails | With Guardrails |

|---|---|---|

| Borrower asks about rates | ”Based on your situation, you’re looking at around 6.2% — pretty competitive right now." | "I can’t quote rates — that requires a full credit and income review with your loan officer. Want me to get that scheduled?” |

| Borrower asks if they qualify for FHA | ”Sounds like you’d likely qualify for FHA with that credit score." | "Qualification depends on several factors your loan officer will verify. I can capture your details and connect you with the right person today.” |

| Borrower asks about a discontinued product | ”Yes, that program is still available — it’s one of our more popular options." | "Let me connect you with someone who can confirm current product availability for your situation.” |

| Borrower asks for a compliance guarantee | ”This process is fully compliant with all federal mortgage regulations." | "Our process is designed to support compliance workflows. Your loan officer can walk you through the regulatory details.” |

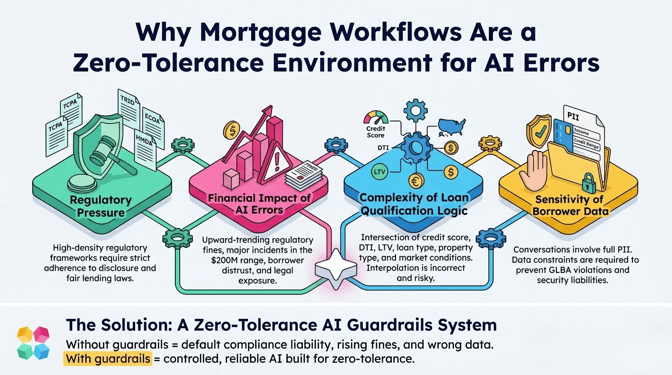

Why Mortgage Workflows Are a Zero-Tolerance Environment for AI Errors

Most industries can absorb a small rate of AI errors as a cost of automation. Mortgage can’t. Here’s why the tolerance threshold in lending is effectively zero.

Regulatory Pressure: TCPA, TRID, ECOA, HMDA, and Fair Housing

The mortgage industry operates under one of the densest regulatory frameworks in US financial services. The Truth in Lending Act and TRID requirements govern how loan terms are disclosed.

ECOA prohibits discriminatory lending decisions. HMDA requires detailed reporting. The Fair Housing Act creates fair-lending obligations around how leads are engaged and qualified.

An AI that operates without guardrails in this environment isn’t just risky — it’s a compliance liability by default. The AI doesn’t know about TRID. It doesn’t understand ECOA. Without explicit constraints, it will respond in ways that create exposure — not because it’s malicious, but because it’s unconstrained.

Financial Impact of Incorrect Information

The downstream costs of AI errors in mortgage compound fast. Regulatory fines for AI-enabled misinformation in financial contexts are trending upward, with major incidents carrying penalties in the $200M range. Beyond fines: borrower distrust drives drop-off, incorrect qualification logic wastes LO time on non-viable leads, and misleading statements create legal exposure at the individual case level.

Complexity of Loan Qualification Logic

Mortgage qualification isn’t a single calculation. It’s an intersection of credit score, DTI, LTV, loan type, property type, state guidelines, lender overlays, and current market conditions. No general-purpose AI has accurate, up-to-date knowledge of all these variables. An unguarded AI will interpolate — and the interpolation will be wrong in ways that aren’t obvious until they cause problems.

Sensitivity of Borrower Data

Mortgage conversations involve PII at every turn: income figures, credit ranges, employment history, property addresses, loan amounts. An AI without data constraints will reference, repeat, and in some cases inadvertently expose this information in ways that violate GLBA and create data security liability.

| Key insight: In mortgage, the AI isn’t just a conversation tool. It’s a regulated touchpoint. Every message it sends has the potential for compliance, fair lending, and data privacy implications. That’s the environment guardrails are built for. |

What Are AI Guardrails? An Operational Definition for Enterprise Teams

The word ‘guardrails’ gets used loosely in AI marketing. For enterprise mortgage teams evaluating AI Sales Agents, here’s a precise definition that matters operationally.

AI guardrails are hard constraints on AI behavior — not soft suggestions, not prompts, not hoped-for outcomes. They operate at the architecture level, controlling what the AI can say, what data it can access, and what actions it’s permitted to take. Three layers make up a complete guardrail system:

Layer 1: Behavioral Constraints — What the AI Is Allowed to Say

These are explicit rules about permitted and prohibited responses. Examples in a mortgage context:

- The AI cannot quote rates, APRs, or monthly payment estimates

- The AI cannot make eligibility determinations or approval statements

- The AI must include specific disclosures when discussing loan types

- The AI must escalate to a human for any question involving specific financial advice

- The AI cannot use language that implies a guarantee or committed outcome

Behavioral constraints override persona, override prompts, and override any instruction in the conversation. They’re non-negotiable.

Layer 2: Data Constraints — What the AI Is Allowed to Use

Grounding constraints determine which information the AI can draw on when generating responses. A grounded AI only responds from its approved knowledge base: verified product information, current compliance content, approved FAQs, and escalation protocols. If information isn’t in the approved knowledge base, it doesn’t exist for that AI.

This is the primary technical mechanism that prevents hallucination. An AI that can only respond from verified data cannot fabricate rates, invent products, or cite regulations that don’t apply. The constraint isn’t a filter applied after the fact — it’s a limitation on what the model can access when generating its response.

Layer 3: Action Constraints — What the AI Is Allowed to Do

In an AI Sales Agent context, the AI isn’t just generating text — it’s triggering workflows. It can capture lead data, initiate follow-up sequences, schedule appointments, and route conversations to human reps. Action constraints define exactly which of these are permitted and under what conditions.

What a properly constrained AI Sales Agent should not be able to do:

- Simulate or imply a loan approval or pre-qualification decision

- Commit to a rate lock or product availability

- Modify borrower records or submit applications

- Make any representation that requires a licensed mortgage professional

| Guardrails are a control system, not a feature. The difference matters: a feature can be toggled. A control system is the infrastructure that makes everything else safe to run. |

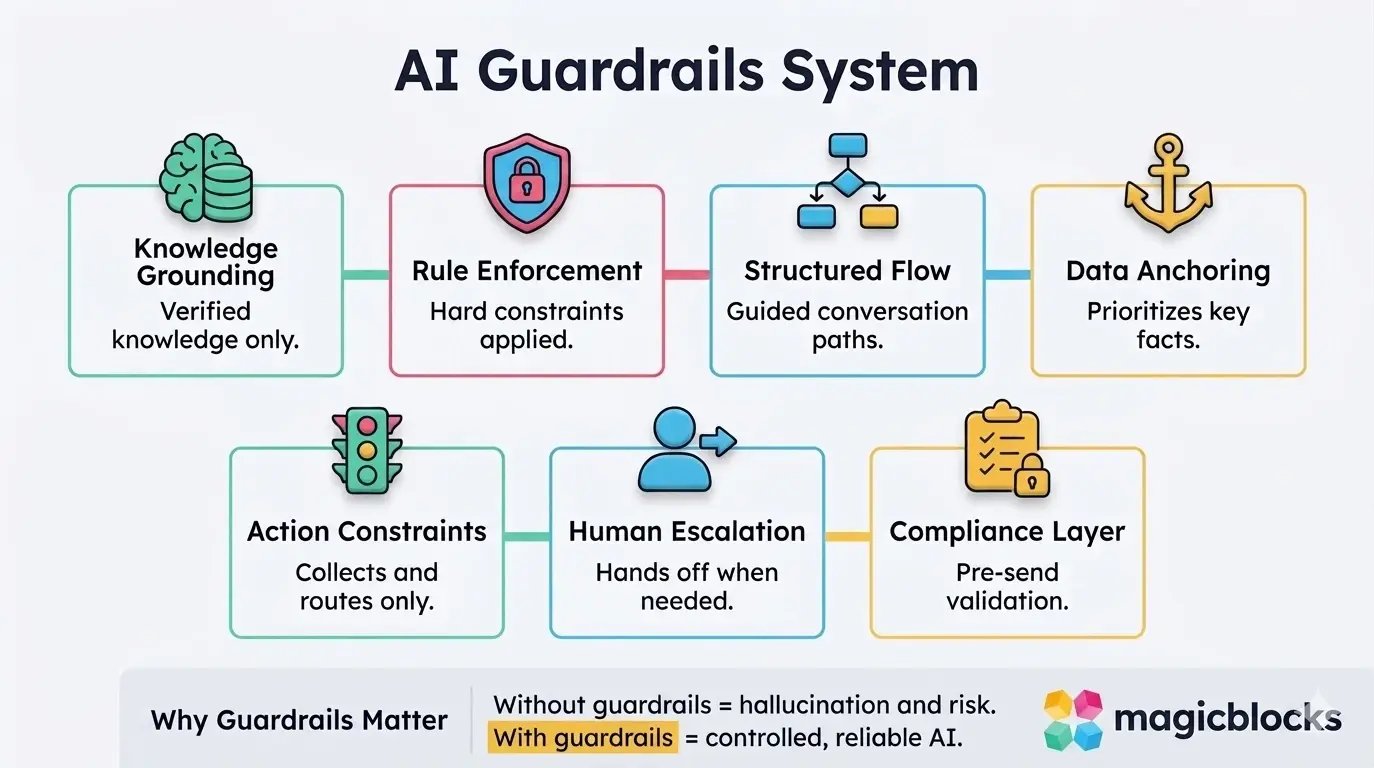

The 7 Core Guardrails That Prevent Hallucinations in Mortgage AI

These aren’t theoretical. This is the architecture required to deploy AI in mortgage workflows without creating compliance exposure.

1. Knowledge Grounding: The Anti-Hallucination Foundation

Every response the AI generates must be drawn from a verified, controlled knowledge base — approved product documentation, compliance content, FAQs, and escalation protocols. Nothing else.

In MagicBlocks, the Knowledge Base is the foundational layer of every AI Sales Agent. It’s where mortgage-specific product rules, eligibility criteria, disclosure language, and compliance content live. The Sales Playbook sits alongside it — teaching the agent how to sell, how to handle objections, and how to advance the conversation — but the knowledge boundary is explicit. If it’s not in the knowledge base, it shouldn’t exist in the conversation.

This matters because it closes the primary hallucination pathway. A grounded AI can’t fabricate what it can’t access.

2. Explicit Rule Enforcement

Grounding alone isn’t sufficient. Rule enforcement adds hard constraints on top of knowledge grounding: specific prohibitions that the AI must observe regardless of what a borrower asks or how persistently they push.

In mortgage, standard explicit rules include:

- No rate quoting without LO authorization and credit validation

- No eligibility statements without proper qualification workflows

- Mandatory disclosure language when discussing specific loan types

- Immediate escalation triggers for compliance-sensitive questions

- No engagement with requests that cross into financial advice

This is the shift from ‘AI that answers everything’ to ‘AI that knows when not to answer.’ The second type is the only one that belongs in mortgage.

3. Structured Conversation Architecture

Free-form conversational AI is dangerous in regulated environments. An AI that can wander into any topic will, eventually, wander into liability.

Structured conversation architecture means the AI operates within a defined journey — a logical flow from engagement through qualification to conversion or escalation.

The Dynamic Journey Engine in MagicBlocks is built on this principle: it computes the next best action in real time based on relationship state, lead behavior, and lifecycle position, within a defined set of permitted paths. It can adapt, but it cannot leave the structure.

The practical effect: structure reduces hallucination more reliably than prompts do. Prompts say ‘please stay on topic.’ Structure makes off-topic responses architecturally unavailable.

4. Key Facts and Data Anchoring

Separate from the general knowledge base, anchored data is the set of specific facts the AI always has access to and always prioritizes: current product availability, company contact information, verified eligibility parameters, mandatory disclosure language, and escalation contacts.

MagicBlocks calls these Priority Knowledge — the first layer the AI references before drawing on anything else. Anchoring prevents memory drift, response inconsistency, and the scenario where the AI gives one answer in conversation 1 and a different answer in conversation 47.

5. Action-Level Constraints: Execution Control

In a mortgage funnel, the AI Sales Agent’s job is to collect, qualify, and route. Not to decide. Action constraints enforce this boundary precisely.

The AI can:

- Collect borrower information through structured questions

- Trigger qualification workflows and schedule LO appointments

- Route conversations to the right human at the right time

- Log interaction data and update CRM records

The AI cannot:

- Fabricate approval signals or pre-qualification language

- Simulate loan decisions or product commitments

- Submit applications or initiate underwriting processes

- Represent itself as a licensed mortgage professional

This boundary between data collection and decision-making is the line between an AI Sales Agent and a compliance risk.

6. Human-in-the-Loop Escalation

The safest AI knows when to stop talking and hand off to a human. Escalation isn’t a fallback — it’s a designed part of the architecture.

Trigger conditions for mandatory escalation in a mortgage AI deployment:

- Any question about specific rates, APRs, or payment calculations

- Eligibility questions that require licensed interpretation

- Compliance-sensitive scenarios (fair lending, ECOA situations, hardship)

- Borrower frustration signals or explicit requests for a human

- Any scenario where the AI’s response would require licensed knowledge

The standard MagicBlocks architecture includes 76% of enterprises already include human-in-the-loop processes as a safeguard against AI errors — the escalation trigger is how that becomes automatic rather than reactive.

7. Compliance and Security Guardrails: The Invisible Layer

This layer operates underneath every conversation. In MagicBlocks, it’s called Guardian AI — a dedicated second AI model that reviews every outbound message for compliance, brand safety, and business rule violations before it sends, and auto-rewrites anything that breaks the rules.

What Guardian AI covers in a mortgage deployment:

- TCPA and DNC compliance: quiet hours, opt-in/opt-out requirements, suppression lists

- Jailbreak prevention: multi-layer prompt injection protection that blocks attempts to bypass constraints

- PII auto-redaction: credit scores, income figures, SSNs, and account details are identified and handled per GLBA requirements

- Brand voice enforcement: declarative rules applied to every message without requiring prompt engineering

- Audit trail generation: every interaction logged for compliance review

Most AI deployments in mortgage rely on post-hoc review — someone checks outputs after the fact. Guardian AI pre-screens before sending. That architecture difference is what makes enterprise deployment viable in regulated industries.

| MagicBlocks certifications: SOC 2 (Enterprise) and ISO 27001:2022 — verified at trust.magicblocks.ai. Enterprise deployments include edge compute with geo-optimized routing for latency and data residency requirements. |

How Guardrails Work Together: End-to-End Mortgage Flow

Without Guardrails: The Failure Scenario

A borrower asks: ‘What rate can I get for a 30-year fixed?’ The unguarded AI answers with a fabricated number. It sounds plausible. The borrower builds expectations around it. The LO gets a call from a prospect expecting 6.1% in a 6.8% environment. The relationship is damaged before it started.

With Guardrails: The Controlled Flow

The same query in a properly architected AI Sales Agent:

- Query received: ‘What rate can I get for a 30-year fixed?’

- Knowledge check: Rate quoting is not in the approved knowledge base. Explicit rule triggered: no rate statements without LO authorization.

- Guardian AI pre-screen: Response validated against TCPA rules, brand voice, and compliance constraints.

- Structured response generated: ‘Rates depend on your credit profile, loan amount, and current market conditions — your loan officer can give you accurate numbers after a quick review. Want me to get that scheduled for you?’

- Action triggered: Appointment booking or LO handoff initiated. Data captured for CRM.

The borrower gets a helpful response. No compliance exposure. The LO gets a warm handoff with context. That’s the architecture working.

Why Most ‘AI Chatbots’ Fail in Mortgage Use Cases

Generic conversational AI tools — even sophisticated ones — aren’t built for mortgage. They’re built for conversation. Those are different objectives.

Conversation is optimized for engagement: keep the user talking, answer questions, sound helpful. Mortgage conversion is optimized for qualification, compliance, and handoff. The failure modes of chatbots in mortgage are predictable:

- No knowledge grounding: The AI draws on its general training data, which includes unreliable, outdated, and contradictory mortgage information from the open web

- No rule enforcement: There’s no mechanism that prevents the AI from quoting rates, making eligibility statements, or engaging with compliance-sensitive questions

- No structured journey: The AI follows the conversation wherever it goes, including off-topic, off-compliance, and off-brand directions

- No compliance layer: There’s no pre-send screening. TCPA rules, PII handling, and audit trails are not part of the architecture

The result: 39% of AI-powered customer service bots were pulled back or reworked in 2024 due to hallucination-related errors. In mortgage, that’s not an acceptable iteration cycle.

An AI Sales Agent in the MagicBlocks category is a fundamentally different architecture. It’s built for conversion and compliance from the ground up — not retro-fitted with filters.

Guardrails vs. Prompts: What Actually Prevents Hallucinations

This is a common misconception worth addressing directly. Mortgage teams that have experimented with GPT-based tools often try to solve hallucination problems by engineering better prompts. It helps. It doesn’t fix it.

| Prompts | Guardrails | |

|---|---|---|

| Type | Soft guidance | Hard constraints |

| Enforcement | Probabilistic — the model may or may not follow | Architectural — the model cannot violate |

| Hallucination prevention | Reduces frequency | Prevents at the source |

| Compliance reliability | Inconsistent | Systematic |

| Enterprise suitability | Insufficient for regulated industries | Required for regulated industries |

The distinction in plain language: prompts influence what the AI tends to say. Guardrails control what it’s allowed to say. For a regulated sales environment where a single wrong statement creates legal exposure, tendency isn’t good enough.

| Prompts influence behavior. Guardrails control it. In mortgage, you need control. |

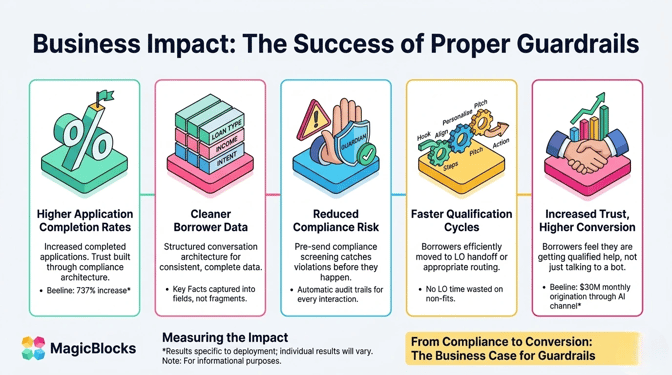

Business Impact: What Happens When You Get Guardrails Right

Enterprise mortgage operations that deploy AI Sales Agents with proper guardrail architecture see measurable improvements across the funnel — not just in compliance, but in conversion.

Higher Application Completion Rates

Beeline’s deployment of MagicBlocks’ AI Sales Agent produced a 737% increase in completed applications (results specific to that deployment and implementation; individual results will vary). The compliance architecture was part of what made that trust possible.

Cleaner Borrower Data

Structured conversation architecture means data collection is consistent and complete. MagicBlocks captures Key Facts — loan type, income range, timeline, borrower intent — in structured fields rather than unstructured chat. That data flows into Encompass, HubSpot, GoHighLevel, or Salesforce clean, not in free-text fragments.

Reduced Compliance Risk

Pre-send compliance screening catches violations before they happen. The Guardian AI architecture means your compliance team isn’t reviewing transcripts after the fact looking for problems — it means the problems don’t make it into the transcript. Audit trails are generated automatically for every interaction.

Faster Qualification Cycles

The HAPPA Framework (Hook, Align, Personalise, Pitch, Action) built into every MagicBlocks AI Sales Agent is designed to advance qualification efficiently. Borrowers who are a fit get moved toward LO handoff. Borrowers who aren’t get routed appropriately. Neither group wastes LO time. MagicBlocks deployments achieve a 48.72% conversation-to-lead rate on the web chat channel (Beeline deployment, specific results vary by implementation and market).

Increased Trust, Higher Conversion

This is the conversion effect that most mortgage ops teams underestimate. Borrowers who interact with a compliant, accurate, appropriately scoped AI don’t feel like they’re talking to a bot that’s going to get them in trouble. They feel like they’re getting qualified help. That trust converts. Beeline’s deployment reached $30M in monthly origination volume through the MagicBlocks AI sales channel — results specific to that deployment; individual outcomes will vary based on market, implementation, and team.

How to Evaluate AI Guardrails in Mortgage Platforms: A Checklist

If you’re assessing AI Sales Agent vendors for a mortgage deployment, here are the questions that matter. Any vendor that can’t answer these with specifics is operating without the architecture you need.

| Evaluation Question | What to Look For |

|---|---|

| Does the AI only respond from approved knowledge? | Knowledge base architecture with explicit grounding — not general training data |

| Can you define ‘do not answer’ rules? | Explicit rule enforcement with hard constraints, not just prompt instructions |

| Is the conversation structured or free-form? | Journey-based architecture with defined paths — not open-ended chat |

| Are actions controlled or open-ended? | Explicit action constraints with clear boundaries on what the AI can trigger |

| Is escalation built into the architecture? | Defined trigger conditions for human handoff, not just an option |

| Are compliance rules enforced before sending? | Pre-send screening (like Guardian AI) — not post-hoc review |

| Is PII handling documented? | Explicit PII auto-redaction with audit trail capability |

| What are the certifications? | SOC 2 and ISO 27001 for enterprise deployments in regulated industries |

If a vendor answers ‘yes’ to all of these but can’t show you the architecture behind the answer, keep asking. The controls either exist or they don’t. Marketing language about ‘compliance-aware AI’ without mechanism specifics is a prompt dressed up as a guardrail.

The Future: From Chatbots to Controlled AI Sales Systems

The mortgage industry is at an inflection point with AI. The first wave of deployments — generic chatbots bolted onto websites — is producing the compliance incidents and borrower trust problems that were predictable. The second wave is the controlled AI Sales Agent: purpose-built for conversion, constrained for compliance, architected for enterprise deployment.

The shift is from:

- Chatbot to AI Sales Agent: from conversation to conversion-optimized selling

- Prompt to guardrail: from soft guidance to hard constraints

- Post-hoc review to pre-send screening: from reactive to proactive compliance

- Generic AI to vertically grounded AI: from general training data to verified mortgage knowledge

Guardrails will move from differentiator to baseline requirement. Enterprise mortgage operations — lenders running thousands of leads per month, enterprise teams managing complex compliance environments, regional banks with multi-state regulatory obligations — will require documented guardrail architecture as a precondition for vendor evaluation.

MagicBlocks is built for this environment. The AI Sales Agent category exists precisely because conversion and compliance aren’t competing objectives. With the right architecture, they reinforce each other.

Create an AI Sales Agent at magicblocks.ai

FAQ

What causes AI hallucinations in mortgage workflows?

Hallucinations occur when an AI responds from statistical prediction rather than verified data. In mortgage, the risk is amplified because accurate responses require current product knowledge, borrower-specific data, and regulatory awareness — none of which a general-purpose AI has. The primary cause is the absence of knowledge grounding.

How do AI guardrails prevent compliance violations?

Guardrails create hard constraints on AI behavior at the architecture level. Explicit rules prohibit rate quoting, eligibility statements, and compliance representations. Knowledge grounding limits responses to verified content. Pre-send screening (Guardian AI) catches violations before they reach the borrower. Together, these layers prevent the specific response types that create compliance exposure.

Can AI safely quote mortgage rates?

No. Rate quoting requires current market data, credit verification, and LO authorization that no AI system should simulate without those inputs. A properly architected AI Sales Agent declines rate questions and routes to a human, capturing the borrower’s data for the LO handoff instead.

What’s the difference between AI guardrails and prompts?

Prompts are instructions — the AI may or may not follow them. Guardrails are architectural constraints — the AI cannot violate them. In a regulated environment, the distinction is material. Prompts reduce hallucination frequency. Guardrails prevent specific hallucination types by making them architecturally unavailable.

Do all AI Sales Agents include guardrails?

No. The term ‘AI Sales Agent’ is used across a wide range of products, many of which are generic chatbots with sales-oriented prompts. A genuine enterprise AI Sales Agent for mortgage should have documented knowledge grounding, explicit rule enforcement, structured conversation architecture, pre-send compliance screening, and certified data security. See how MagicBlocks compares to alternatives — ask vendors for the architecture, not the marketing.

How do you test if an AI system is hallucinating?

Standard testing approaches include adversarial prompting (asking questions the AI shouldn’t answer), rate and eligibility queries to see if the AI fabricates specifics, edge case borrower scenarios, and compliance-sensitive questions. Enterprise teams should also review transcripts for confidence-versus-accuracy alignment — confident wrong answers are the hallucination signature. MagicBlocks includes a ‘Try My Agent’ testing environment for this purpose.

What industries require strict AI guardrails?

Mortgage, insurance, financial services, healthcare, and legal are the highest-priority categories — industries where inaccurate AI output creates regulatory, financial, or safety consequences. In these verticals, guardrail architecture isn’t optional. It’s the precondition for responsible deployment.

Want to see this in action?

See a demoRead the playbook. Now see it run.

Watch a 4-minute demo. No sales pitch. Then decide if you want to talk.