The Enterprise AI Transformation Guide for Mortgage Lenders

How enterprise lenders are deploying AI Sales Agents to close the conversion gap — and what it actually takes to scale.

Discover how mortgage lenders can harness AI Sales Agents to enhance conversion rates, streamline processes, and drive revenue in a competitive landscape.

On this page 15

- Top Challenges Mortgage Organizations Face When Integrating AI

- Key Considerations to Accelerate AI Adoption and Long-Term Value

- What Is Enterprise AI Transformation in Mortgage Lending?

- Why Enterprise AI Transformation Matters for Mortgage Lenders

- Key Components of AI Transformation in Mortgage Lending

- How Enterprise AI Transformation Works (Mortgage Context)

- AI Transformation vs. Digital Transformation in Mortgage

- How AI Transforms Mortgage Lenders’ Lead Conversions

- How Enterprise Mortgage Lenders Are Implementing AI Sales Agents in 2026

- What Is the ROI of Enterprise AI Transformation?

- How to Measure Success Across AI Adoption, Efficiency, Quality, and Satisfaction

- AI Transformation Readiness Checklist for Mortgage Lenders

- Conclusion: The Conversion Gap Is a Choice

- Frequently Asked Questions

How enterprise lenders are deploying AI Sales Agents to close the conversion gap — and what it actually takes to scale.

| TL;DR Enterprise AI transformation in mortgage lending means embedding AI Sales Agents across the borrower lifecycle to drive conversion and efficiency. Most lenders fail because they stay stuck in pilot mode, lack unified data, and never tie AI to real revenue outcomes. The ones pulling ahead are deploying AI Sales Agents that engage instantly, qualify intelligently, and follow up without dropping the ball. |

You’ve sat in enough pipeline reviews to know the feeling. The leads came in. The team had a good month generating them. But somewhere between form fill and funded loan, a chunk of that pipeline just… vanished.

Not because borrowers weren’t interested. Because no one got to them fast enough, followed up consistently enough, or qualified them well enough before burning human hours on the wrong ones.

That’s not a lead generation problem. That’s a conversion problem. And in 2026, enterprise mortgage lenders who haven’t figured that out are leaving serious origination volume on the table.

This guide breaks down exactly what enterprise AI transformation means for mortgage lenders — what the research says, what the architecture looks like, and how the lenders who are actually moving the needle are doing it.

Top Challenges Mortgage Organizations Face When Integrating AI

Let’s start with the uncomfortable truth. According to McKinsey’s State of AI research, most organizations report AI adoption — but very few capture value at scale. The mortgage industry is no exception.

1. Failure to Scale Beyond Pilots

This is the most common and most expensive failure mode. A lender runs a proof of concept — maybe an AI chatbot on their website, maybe a lead scoring experiment in the CRM. It works well enough to get executive buy-in.

Then six months later, it’s still a pilot. No production rollout. No revenue impact. Just a vendor on the monthly invoice and a slide deck in the QBR.

McKinsey’s enterprise transformation research identifies this as the single biggest gap between AI adopters and AI leaders: the ability to move from POC to production to enterprise-wide deployment. Most organizations get stuck at step two.

2. Fragmented Data Ecosystems

Your LOS, CRM, and servicing systems weren’t built to talk to each other. That means your AI has no unified borrower view. It can’t see that the lead who just filled out a rate inquiry also refinanced with you in 2021, called the servicing line twice last quarter, and has an ARV that makes them an ideal HELOC candidate.

The KPMG Banking AI Blueprint identifies fragmented data as one of the primary barriers to AI value creation in financial services. You can’t optimize what you can’t see.

3. Lack of Clear Value Linkage

AI initiatives that aren’t tied to specific revenue, conversion, or cost metrics die in committee. When leadership can’t see a direct line between the AI deployment and funded loans or cost-per-application reduction, the budget conversation gets uncomfortable fast. The initiative stays alive long enough to spend the budget, then gets quietly shelved.

4. Trust, Risk, and Compliance Barriers

Mortgage is a regulated industry. TRID, ECOA, HMDA, Fair Housing Act, GLBA — these aren’t optional considerations. They’re the floor. The KPMG blueprint specifically calls out trust and governance as the make-or-break factor for AI adoption in banking and lending. Compliance teams that can’t validate AI outputs before they reach borrowers won’t let those systems anywhere near production. That’s not obstruction. That’s risk management.

5. Operating Model Gaps

AI doesn’t run itself. Who owns the AI Sales Agent deployment? Who calibrates it when conversion drops? Who reviews compliance flags? Most mortgage organizations don’t have answers to these questions. The technology gets deployed but the organizational structure to manage it doesn’t exist yet.

| The symptoms are familiar: low conversion rates, slow response times, loan officers chasing cold leads, and a CRM full of borrowers who went elsewhere. The root cause is almost always one of these five gaps. |

Key Considerations to Accelerate AI Adoption and Long-Term Value

The Stanford Enterprise AI Playbook is clear on this: sustainable AI value capture requires operating model change, not just technology deployment. Here’s what that looks like in practice for mortgage lenders.

Design an AI Strategy Aligned with Core Lending Competencies

Focus on the highest-leverage use cases first: origination, underwriting support, and borrower engagement. Don’t start with back-office automation when your conversion funnel is leaking 60% of qualified leads before a loan officer ever makes contact. Fix the revenue problem first.

For enterprise lenders running multiple products (purchase, refinance, HELOC, jumbo), prioritize the use cases where response time and follow-up consistency have the biggest impact on funded loan rate. That’s almost always the purchase origination funnel.

Build Trust Into the Transformation Roadmap

Explainability isn’t optional in mortgage. If your AI is making recommendations that affect credit decisions, your compliance team needs to understand why.

The KPMG blueprint recommends embedding governance frameworks from day one, not retrofitting them after deployment. Compliance teams that are involved early don’t slow down deployment — they protect it.

Create Sustainable Data and Technology Infrastructure

A unified borrower data layer is the foundation of everything else. Without it, your AI Sales Agent is working blind — engaging leads without context, qualifying without history, following up without knowing what the borrower already told someone else on your team. API-first architecture that connects your LOS, CRM, and AI layer is the infrastructure investment that makes everything else possible.

Build a Culture That Uses AI to Uplift Human Potential

The Stanford Enterprise AI Playbook frames this as the central operating model shift: AI handles the repeatable work, and humans focus on the high-judgment decisions. For mortgage, that means AI Sales Agents handle initial engagement, qualification, and follow-up sequences — and loan officers spend their time on borrowers who are actually ready to move forward.

Organizations that deploy this model have seen loan officers focus more time on qualified borrowers, which can contribute to improved funded loan rates. Results depend on deployment quality, lead volume, and team adoption.

What Is Enterprise AI Transformation in Mortgage Lending?

| Definition: Enterprise AI transformation in mortgage lending is the process of embedding AI Sales Agents across the borrower lifecycle — from lead acquisition to loan closing — to improve conversion rates, operational efficiency, and compliance at scale. It’s not a technology project. It’s a revenue strategy. |

The distinction matters. Digital transformation was about digitizing existing processes — moving paper applications online, automating document collection, building borrower portals. AI transformation is different.

It’s about optimizing the decisions inside those processes: who to engage first, how to qualify efficiently, when to follow up, and how to keep a borrower moving through the funnel without dropping the relationship. For a full breakdown of the mechanics, see what is AI lead conversion.

At the enterprise level, this means AI operating across thousands of leads simultaneously, maintaining conversation context across channels, qualifying in real time, and handing off only the right borrowers to the right loan officers at the right moment. The AI Sales Agent becomes the conversion layer between your lead generation and your human sales team.

Why Enterprise AI Transformation Matters for Mortgage Lenders

McKinsey’s State of AI research shows a clear and widening gap between organizations capturing AI value at scale and those stuck in pilot mode.

In a rate-sensitive market where purchase origination is competitive and acquisition costs keep climbing, the conversion rate difference between a 3% close rate and a 7% close rate isn’t marginal. It’s the difference between a profitable origination operation and one that’s burning budget on leads that go nowhere.

| → Lenders with AI-assisted engagement report faster lead response times — in some deployments, under 60 seconds vs. the 8-12 minute industry average → Organizations that tie AI to specific conversion metrics see higher ROI from their deployment than those treating AI as a cost-reduction exercise → The risk of inaction: AI-native lenders and fintechs are already competing with response times and personalization that traditional manual workflows can’t match → Rising CAC makes the conversion math increasingly punishing — paying $45-80 per lead and closing 3% is a different business than paying the same and closing 7% |

The McKinsey enterprise transformation framework identifies competitive advantage, CAC reduction through better qualification, faster decision-making, and new revenue through personalization as the primary value drivers. In mortgage, all four show up directly in funded loan volume.

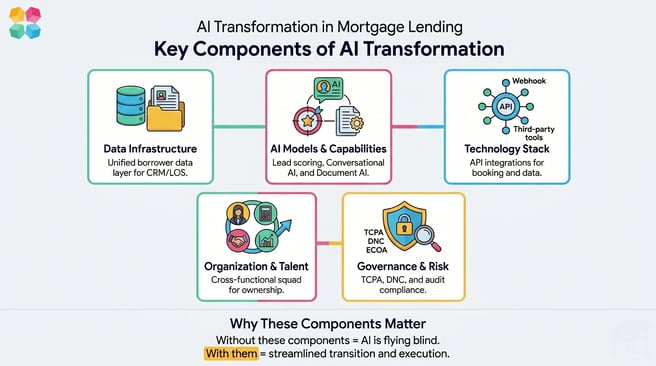

Key Components of AI Transformation in Mortgage Lending

Drawn from the KPMG Banking AI Blueprint and Stanford Enterprise AI Playbook, here are the five components that enterprise mortgage transformations can’t skip:

1. Data Infrastructure

A unified borrower data layer that consolidates LOS, CRM, and marketing data. Without it, your AI is flying blind. With it, your AI Sales Agent knows every touchpoint a borrower has had with your organization — and can engage them accordingly.

2. AI Models and Capabilities

Lead scoring tells your team who to prioritize. Conversational AI handles the engagement and qualification work. Document AI accelerates the processing side. These aren’t separate initiatives — they’re components of the same conversion architecture.

3. Technology Stack

A well-connected integration layer determines how effectively your AI Agent can support end-to-end workflows. MagicBlocks enables connections to external systems through APIs, webhooks, and third-party tools, allowing actions like sending lead data, triggering automations, and booking meetings. By linking your AI Agent to the rest of your tech stack, you can streamline the transition from conversation to execution while maintaining a consistent user experience.

4. Organization and Talent

Who owns this? AI center of excellence structures work for organizations large enough to support them. For most enterprise lenders, the practical answer is a cross-functional squad with representation from operations, compliance, marketing, and loan officer leadership — with clear ownership of performance metrics.

5. Governance and Risk

Responsible AI in mortgage means TCPA and DNC compliance for outreach, ECOA compliance for qualification logic, and audit trails for every AI interaction that could affect a credit decision. This isn’t a compliance team checkbox — it’s the architecture that keeps enterprise deployments in production.

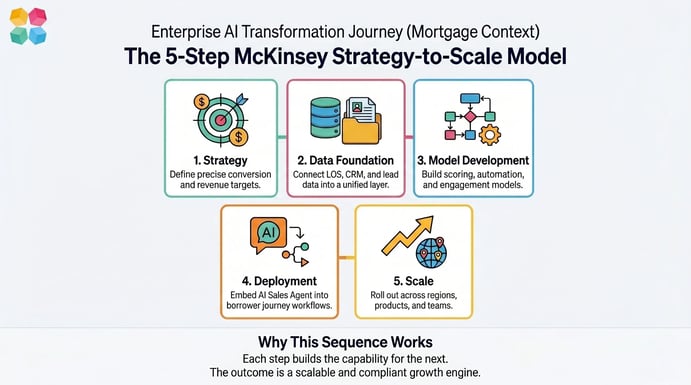

How Enterprise AI Transformation Works (Mortgage Context)

The McKinsey strategy-to-scale model maps cleanly onto the mortgage origination context. Here’s what the five-step progression looks like in practice:

Step 1: Strategy — Define Conversion and Revenue Targets

Start with the business outcome, not the technology. What funded loan volume increase would justify this investment? What response time do you need to be competitive in your primary markets? What’s the current cost per qualified application, and where do you need it to be? These are the numbers your AI transformation gets measured against.

Step 2: Data Foundation — Integrate Borrower and Operational Data

Connect your LOS, CRM, and lead sources into a unified borrower data layer. Every lead that comes in — from Zillow, LendingTree, your own website, a realtor referral — needs to flow into a single system where the AI can see the full picture. This step takes longer than people expect. It’s also what separates deployments that actually work from ones that underperform.

Step 3: Model Development — Build Scoring, Automation, and Engagement Models

Lead scoring models prioritize by intent and qualification signals. Engagement models determine the right hook for each borrower segment — a first-time homebuyer getting a rate inquiry from a Zillow ad is a different conversation than a repeat customer checking HELOC rates at 9pm. Automation models handle the follow-up sequences that human teams never consistently execute.

Step 4: Deployment — Embed AI Into Workflows

This is where the AI Sales Agent goes live in the actual borrower journey. Inbound leads get engaged within 60 seconds. Qualification happens in the chat or SMS conversation before a loan officer is involved. Follow-up runs automatically across 8-12 touches without human intervention. Loan officer handoffs happen with full context already captured.

Step 5: Scale — Roll Out Across Regions, Products, and Teams

A deployment that works in one market or product line gets replicated across the enterprise. This is where the operating model investments pay off — documented playbooks, calibrated agents, and governance frameworks that don’t need to be rebuilt from scratch for each new rollout.

AI Transformation vs. Digital Transformation in Mortgage

The Stanford Enterprise AI Playbook draws a clear distinction that mortgage leaders need to internalize.

| Dimension | Digital Transformation | AI Transformation |

|---|---|---|

| Primary focus | Digitizing existing processes | Optimizing decisions inside processes |

| Automation type | Workflow automation | Predictive and adaptive intelligence |

| Primary output | Faster processing speed | Higher conversion rates |

| Borrower interaction | Self-service portals | Personalized AI conversation |

| Data use | Transaction recording | Behavioral signals and next-best-action |

| Value capture | Cost reduction | Revenue growth + cost reduction |

The key insight: AI transformation is the decision layer on top of your digital infrastructure. You needed digital transformation to build the foundation. AI transformation is what makes that foundation generate revenue.

How AI Transforms Mortgage Lenders’ Lead Conversions

Here’s where the theory meets the pipeline. The McKinsey State of AI research consistently identifies sales and marketing as the highest-ROI AI use cases.

In mortgage, that translates directly into funnel optimization. For a deeper look at how AI Sales Agents drive this, see how AI Sales Agents increase mortgage lead conversion by 6x.

The conversion math illustrates the potential: if you’re spending $50 per lead, receiving 1,500 leads per month, and closing 3%, you’re funding 45 loans. If conversion rates improved to 7% on the same lead spend, that would represent 105 funded loans.

Actual results depend on lead quality, market conditions, team adoption, and deployment configuration. The AI Sales Agent doesn’t replace your team — it helps ensure more lead dollars are working as hard as possible.

Lead Scoring: Who to Prioritize

Not all leads are equal and your loan officers know it. AI lead scoring analyzes intent signals — time of day, page depth, rate comparison behavior, return visits — and surfaces the borrowers most likely to convert today. Your team works the right pipeline instead of dialing through a list sorted by submission time.

Instant Engagement: Responding When Intent Is Highest

A borrower who just submitted a rate inquiry is never more interested than right now. The AI Sales Agent engages within 60 seconds — not the next business morning. It opens with a context-aware message based on what the borrower was looking at, not a generic ‘How can we help?’ That immediate response and relevance is what moves a rate inquiry into a qualified conversation.

Automated Follow-Up: The 8-12 Touch Reality

Industry data shows it takes 8-12 meaningful touches to convert a mortgage lead. Most loan officer teams consistently execute 2-3. The AI Sales Agent handles the rest — structured follow-up sequences across web chat, SMS, and email, calibrated to cadence and borrower response patterns. Every lead gets the follow-up they need, not just the ones who happen to catch a loan officer on a good day.

Application Completion Nudges

Application drop-off is one of the most expensive leaks in the mortgage funnel. A borrower who starts an application and doesn’t complete it didn’t necessarily go somewhere else — they got distracted, got confused, or hit a friction point. AI-triggered re-engagement messages targeting incomplete applications recover funded loans that would otherwise be written off as lost.

| → Conversion rate improvement: from 3% to 5-7%+ on the same lead spend → Time-to-contact: from 8-12 minutes average to under 60 seconds → Follow-up depth: from 2-3 manual touches to 8-12 automated touches per lead → CAC reduction: better qualification means fewer human hours on unqualified borrowers |

How Enterprise Mortgage Lenders Are Implementing AI Sales Agents in 2026

This is where AI transformation stops being a strategy document and starts being a deployment conversation. Here’s what enterprise mortgage lenders are actually building — and what they’re learning along the way.

The Four Leaks That Kill Enterprise Conversion

Every enterprise mortgage lender has the same four holes in their funnel. The Stanford Enterprise AI Playbook frames AI value capture as starting with identifying where the highest-value work is happening and where the most revenue is leaking. In mortgage, that’s always these four points:

- Slow response time: Industry average is 8-12 minutes. By that point, the borrower has submitted two more applications elsewhere.

- Poor qualification: Loan officers spend hours on leads who were never going to close. Meanwhile, qualified borrowers wait.

- Inconsistent follow-up: Human teams can’t maintain 8-12 touches per lead across hundreds of active leads. The follow-up drops off. The lead goes cold.

- Application drop-off: Borrowers who start applications and don’t finish represent funded loans your team never knew they lost.

What AI Sales Agent Deployment Looks Like at Enterprise Scale

MagicBlocks is an AI Sales Agent built specifically for the conversion layer — the gap between lead acquisition and human sales engagement. Here’s what enterprise-scale deployment actually looks like:

The agent runs 24/7 across web chat and SMS, engaging every inbound lead within 60 seconds regardless of volume. It runs the HAPPA framework — Hook, Align, Personalise, Pitch, Action — a five-stage sales methodology developed from the team’s experience across high-intent funnels including mortgage and lending.

At enterprise scale, that means thousands of simultaneous conversations, each one maintaining context, adapting to the borrower’s signals, and moving toward a qualified handoff without human involvement. The Dynamic Journey Engine computes the next best action in real time based on relationship state, lead behavior, and outcome history — not a static flowchart.

For lenders running multiple products across multiple markets, the agent configuration scales horizontally. A purchase lead from a first-time homebuyer gets a different conversation than a refinance inquiry from an existing customer. The agent handles the segmentation automatically.

| Beeline, a digital mortgage lender, deployed an AI Sales Agent built on this architecture. In a defined deployment period on web chat, the results included a 737% increase in completed applications, 484% growth in qualified leads, and a 48.72% conversation-to-lead rate on that channel. These results reflect performance in that specific deployment context. Read the full Beeline case study. Individual results vary based on deployment specifics, lead volume, and market context. |

The Compliance Architecture Enterprise Lenders Actually Care About

This is the section your compliance team will actually read. The KPMG Banking AI Blueprint identifies compliance architecture as the primary trust barrier for AI adoption in financial services. In mortgage, that means building the following into the core architecture, not bolting it on after:

- Pre-send compliance review: Guardian AI reviews outbound messages against TCPA/DNC rules, quiet hours, opt-out requirements, and custom business rules before sending. Messages flagged for potential violations are automatically rewritten to support compliance — reducing the reliance on manual review and helping ensure outreach stays within configured guardrails.

- PII auto-redaction: Credit card numbers, SSNs, and sensitive data are detected and redacted automatically. No manual scrubbing required.

- Audit trails: Every conversation logged and searchable. Compliance teams can review any interaction. Examiners can see exactly what the AI said to every borrower.

- Jailbreak prevention: Multi-layer prompt injection protection prevents borrowers (intentionally or not) from manipulating the AI into making commitments or statements that create compliance exposure.

- Certifications: SOC 2 and ISO 27001:2022 certified for data security. Enterprise-grade infrastructure with geo-optimized edge compute and flexible data residency options. Built with GDPR data-handling principles in mind, including data minimization, access controls, audit logging, and regional data handling to support EU operations. These certifications cover data security practices; lenders remain responsible for their own regulatory compliance obligations.

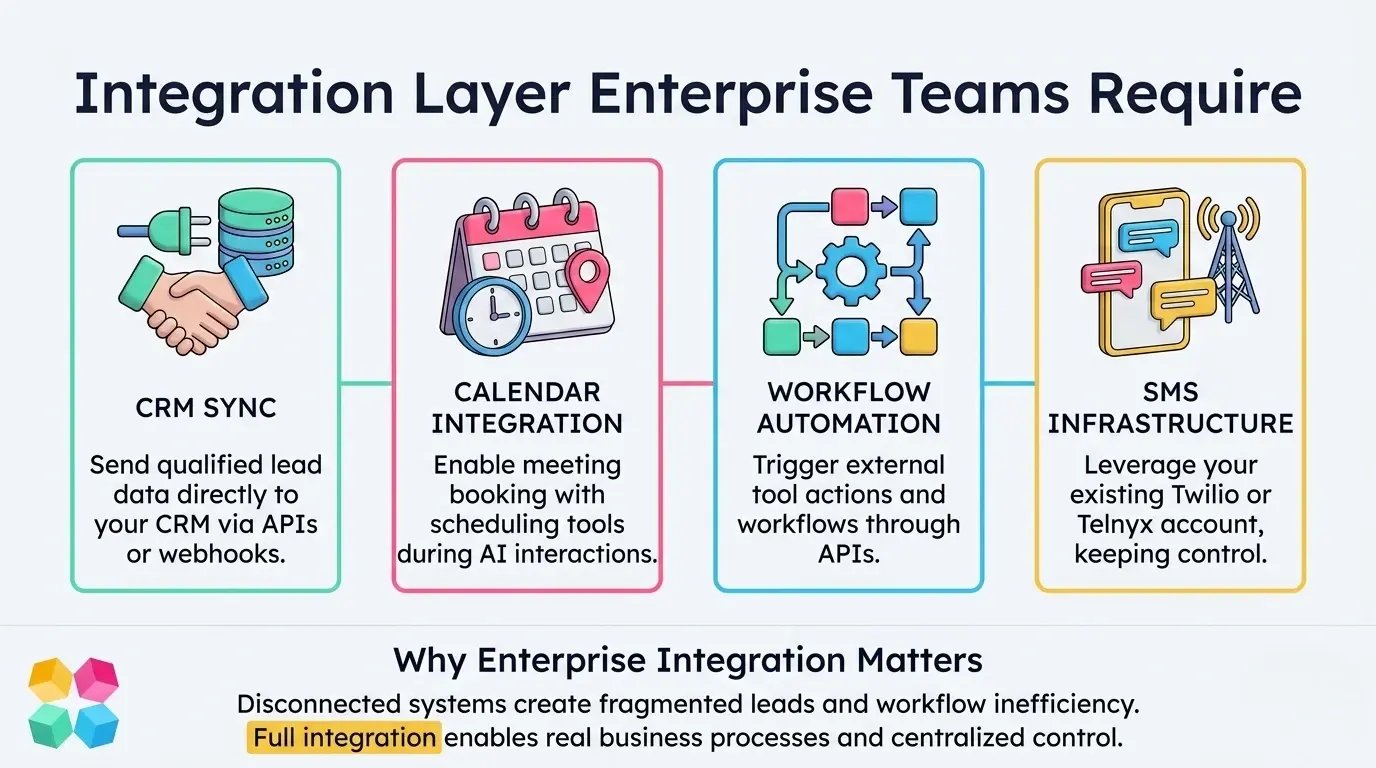

The Integration Layer Enterprise Teams Require

Enterprise deployment without deep integration is just a chat widget with a fancy name. For a full comparison of how leading AI mortgage tools handle integrations, see the best AI tools for mortgage lead generation. The integrations that matter for mortgage lenders:

- CRM sync

MagicBlocks connects with external systems through integrations and webhooks, allowing captured lead data to be sent to your CRM. Using the Actions layer, your AI Agent can pass qualified lead information into connected tools (e.g., via Zapier or other integrations), helping centralize and manage leads within your existing workflow.

- Calendar integration

You can connect scheduling tools like Calendly to enable meeting booking directly within the AI conversation. This allows users to select a time and schedule appointments as part of the interaction flow, streamlining the handoff to your team.

- Workflow Automation via Actions

Through the Library and Actions system, MagicBlocks enables integrations with third-party tools and APIs. These actions can trigger workflows such as sending lead data, booking meetings, or initiating follow-ups, ensuring your AI Agent supports real business processes beyond conversation.

- SMS infrastructure

Lenders bring their own Twilio or Telnyx account. The AI Sales Agent handles the conversation logic; the carrier infrastructure is owned and controlled by the lender. No carrier cost markup.

What the Numbers Look Like at Enterprise Scale

The McKinsey State of AI research shows that AI value capture at enterprise scale is disproportionate to the investment — but only for organizations that actually scale. For industry benchmark data on contact rates, application rates, and funded loan targets, see the 2026 mortgage lead conversion benchmarks. Here’s the range of what the conversion math looks like for enterprise mortgage deployments:

| Metric | Pre-Deployment Benchmark | Post-Deployment Range |

|---|---|---|

| Time-to-contact | 8-12 minutes (industry avg) | Under 60 seconds |

| Qualified lead follow-up depth | 2-3 manual touches | 8-12 automated touches |

| Conversion rate improvement | Baseline (3-4%) | 5-7%+ (results vary by deployment) |

| Agent availability | Business hours | 24/7, no volume ceiling |

| Compliance review | Manual spot-check | Automated pre-send review on all configured outreach |

| Cost per worked lead | $30-80 (human-handled) | Dramatically lower at scale |

The Shift That’s Already Happening

The Stanford Enterprise AI Playbook describes this moment as the transition from reactive to predictive organizations. For mortgage lenders, it plays out in very practical terms. See how AI is transforming mortgage lead generation in 2026 for a detailed breakdown of how top-performing lenders are rebuilding their funnels:

- From reactive to predictive: AI systems identify which borrowers are likely to convert this week based on behavioral signals — before the borrower calls.

- From manual to AI-assisted: Loan officers aren’t dialing through cold lists. They’re taking conversations that are already warm and qualified.

- From volume to velocity: The bottleneck shifts from lead generation to conversion infrastructure. The lenders winning aren’t the ones with the most leads. They’re the ones converting the highest percentage of the leads they already have.

| That correlation isn’t accidental. When repetitive engagement and qualification work is automated, loan officers focus on the conversations that actually require human judgment. The output is more funded loans per loan officer, not just more activity. |

What Is the ROI of Enterprise AI Transformation?

McKinsey’s research identifies a clear ROI gap: most organizations see value in pilots. Few capture value at scale. The difference between the two is almost never the AI itself — it’s whether the deployment was tied to specific business outcomes and scaled across the organization.

The Mortgage ROI Drivers

There are three levers that drive measurable ROI for enterprise mortgage AI deployments:

- Increased funded loans: Better conversion on existing lead spend. Using the same illustrative example — 1,500 monthly leads — moving from a 3% to a 7% close rate would represent 60 additional funded loans. Results vary by deployment, lead quality, and market conditions, but the directional math illustrates why conversion improvement is the highest-leverage ROI driver.

- Reduced manual processing cost: Every lead qualified by AI before loan officer involvement is a reduction in cost per application. For high-volume enterprise lenders, this adds up fast.

- Faster closing cycles: Borrowers who are properly qualified and continuously engaged move through the pipeline faster. Faster cycles mean better pull-through rates and lower per-loan operational costs.

The KPMG Banking AI Blueprint notes that organizations capturing AI value at scale see it in multiple dimensions simultaneously — revenue growth, cost reduction, and risk reduction — because the same system improvement drives all three outcomes.

How to Measure Success Across AI Adoption, Efficiency, Quality, and Satisfaction

The Stanford Enterprise AI Playbook recommends a four-layer KPI framework for enterprise AI deployments. Here’s how it maps to the mortgage context:

| KPI Layer | What to Measure | Mortgage-Specific Metric |

|---|---|---|

| 1. Adoption | % of workflows using AI | % of inbound leads engaged by AI vs. human first touch |

| 2. Efficiency | Time saved per unit | Cost per qualified application, time-to-contact, touches per conversion |

| 3. Quality | Decision accuracy, error reduction | Qualification accuracy rate, compliance violation rate (target: 0) |

| 4. Satisfaction | Borrower and team experience | Borrower response rate to AI engagement, loan officer NPS |

The gut check is always the funded loan number. Everything else — response time, qualification rate, follow-up depth — is a leading indicator. The metric your board cares about is applications submitted and loans funded. Build your KPI framework backward from that.

AI Transformation Readiness Checklist for Mortgage Lenders

Before you deploy, run this checklist. It’s drawn from the combined frameworks of McKinsey, KPMG, and Stanford — applied to the mortgage lending context.

| Readiness Area | What Enterprise Ready Looks Like |

|---|---|

| Strategy | Clear AI roadmap tied to funded loan volume targets, not just ‘improving efficiency’ |

| Data | Unified borrower data layer connecting LOS, CRM, and lead sources |

| Technology | API-first stack with documented integration points for AI layer connectivity |

| Organization | Defined AI ownership with cross-functional representation (ops, compliance, marketing, LO leadership) |

| Governance | Compliance framework reviewed by legal covering TCPA, ECOA, HMDA, and Fair Housing |

| Metrics | Baseline conversion rates, response times, and follow-up depth documented and tracked |

| Pilot to Production Plan | Defined pathway from initial deployment to full enterprise rollout with success criteria at each stage |

| If you can check all seven boxes, you’re ready to deploy. If you can check five, you’re close enough to start the deployment conversation and build toward the gaps. If fewer than five, the work to do is infrastructure and strategy before AI Sales Agent deployment. |

Conclusion: The Conversion Gap Is a Choice

You’re not short on leads. You have a conversion problem. And in 2026, that problem has a concrete solution — AI Sales Agents deployed across the borrower lifecycle, handling the engagement, qualification, and follow-up work that human teams can’t do at scale.

Enterprise mortgage lenders who are winning aren’t doing something magical. They’ve built the data foundation, tied AI to specific revenue outcomes, deployed the compliance architecture their teams can trust, and scaled what works. The result is a funnel where more of the leads they already paid for turn into funded loans.

The lenders who are still deliberating are paying for leads that go to someone who deployed six months ago.

| Create your AI Sales Agent and start converting leads you’ve already paid for. MagicBlocks is a lead conversion engine built specifically for the mortgage industry. Expert-guided deployment, enterprise compliance architecture, and a sales methodology built from the team’s direct experience across mortgage origination funnels. Create your AI Sales Agent at magicblocks.ai |

Frequently Asked Questions

What is enterprise AI transformation in banking?

Enterprise AI transformation in banking is the process of embedding AI-driven decision-making across core banking workflows — from customer acquisition and qualification to underwriting, servicing, and retention. It goes beyond digitizing existing processes. It’s about using AI to optimize the decisions inside those processes at scale, with governance frameworks that satisfy regulatory requirements.

How do mortgage lenders use AI?

Enterprise mortgage lenders are using AI across three primary areas: AI Sales Agents for borrower engagement, qualification, and follow-up in the origination funnel; lead scoring models to prioritize pipeline by conversion likelihood; and document AI to accelerate processing and reduce manual underwriting effort. The highest-ROI deployments focus on the conversion layer — turning more of the leads already in the funnel into funded loans. See how to build a custom mortgage AI agent for a practical walkthrough of deployment.

What is the ROI of AI in lending?

ROI in mortgage AI deployments is driven by three levers: increased funded loan volume from better conversion rates, reduced cost per application from AI-handled qualification, and faster closing cycles from continuous borrower engagement. McKinsey’s research shows that organizations capturing AI value at scale see it across multiple dimensions simultaneously. Individual results depend heavily on lead volume, current conversion baseline, and deployment quality.

What are the biggest challenges in AI adoption?

The top five challenges for mortgage lenders adopting AI are: failure to scale beyond pilots, fragmented data ecosystems that prevent a unified borrower view, lack of clear value linkage to revenue outcomes, trust and compliance barriers in regulated environments, and operating model gaps where no one owns the AI deployment post-launch. Addressing all five is what separates successful enterprise deployments from expensive experiments. Both the KPMG Banking AI Blueprint and McKinsey’s enterprise transformation research identify these patterns consistently across financial services deployments.

Want to see this in action?

See a demoRead the playbook. Now see it run.

Watch a 4-minute demo. No sales pitch. Then decide if you want to talk.